Newsletter – October 2024

The Share Market

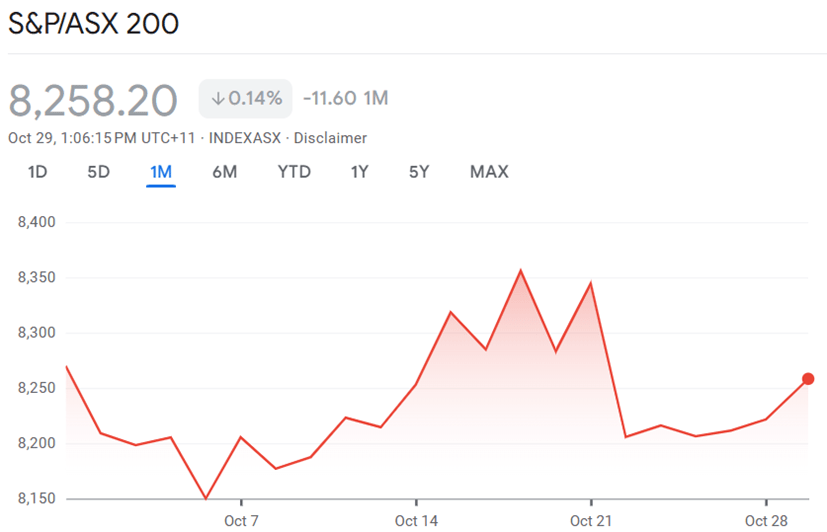

The ASX 200 index experienced fluctuations throughout October. As of October 28, the index was at around 8,250, showing a minute increase of 0.14% for the month. The highest point was around 8,350 on October 21, while the lowest point was around 8,150 on October 7.

The ASX 200's performance in October 2024 reflected a mix of sector-specific movements and broader market trends. While some sectors showed recovery, others faced challenges, leading to fluctuations in the index.

Sector Performance

- Banking and Property: These sectors showed recovery towards the end of the month, with major banks and property stocks driving the market higher.

- Healthcare: Companies like Telix Pharmaceuticals and Sonic Healthcare performed well.

- Mining: Fortescue and Rio Tinto experienced declines due to production updates.

Notable Stocks

- BlueScope Steel: Tumbled 8% after downgrading its guidance due to challenging operating conditions.

- Flight Centre: Analysts see potential for significant returns, predicting a rise of up to 50% over the next 12 months.

- Wisetech Global: Responsible for the majority of the IT sector's losses, with its share price falling significantly.

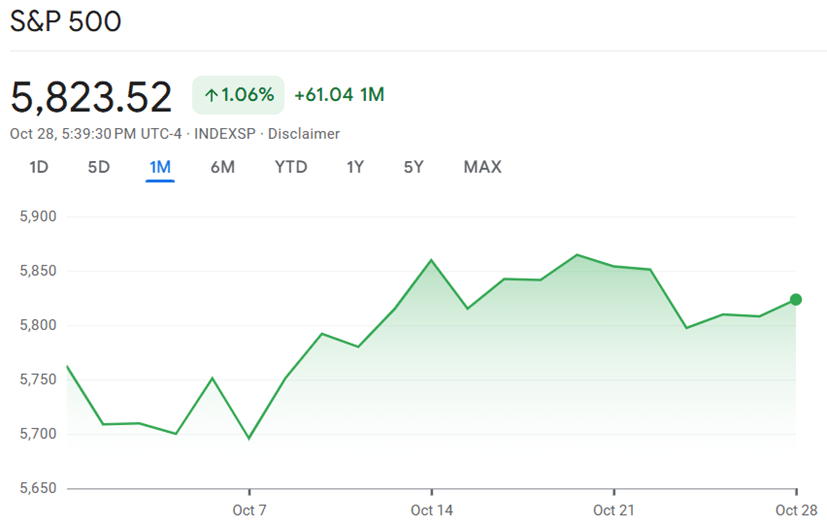

The S&P 500 had a notable performance in October 2024. As of October 28, the index was at 5,823, representing a 1.06% increase for the month. The index reached a peak of 5,880 around mid-October and saw a low of 5,750 at the start of the month.

Influencing Factors

- Artificial Intelligence Stocks: Excitement around AI stocks still contributed to the upward momentum.

- Interest Rates: Falling interest rates also played a role in boosting the index.

- Holiday Spending: Potential stimulus from holiday spending was anticipated to provide a boost to the economy.

The S&P 500 has historically performed well after reaching record highs in October, with an average one-year return of 13.4% following such highs.

The S&P 500 has been on a remarkable run this year, reaching a new all-time high of 5,823 in October 2024, which represents a 23% increase year-to-date. This index has hit 47 record highs in 2024 alone, driven by strong performance in technology stocks and falling interest rates.

In contrast, the ASX 200 has also shown positive performance, but not quite at the same level as the S&P 500. The ASX 200 has delivered an average return of 8.86% per annum over the past ten years, with a solid performance in 2024 as well. However, it has not reached the same heights as the S&P 500, reflecting a more modest growth compared to its US counterpart

While both indices have performed well, the S&P 500's gains have outpaced the ASX 200, highlighting the stronger momentum in the US market this year.

Based on the performance of the S&P 500 and ASX 200 in October 2024, here are some of our thoughts and insights around these markets.

Global Exposure

Investing in both indices can provide a balanced portfolio with exposure to both the US and Australian markets. The S&P 500 offers global reach with companies like Apple, Microsoft, and Amazon, while the ASX 200 provides strong representation from sectors like banking, mining, and healthcare.

Sector Performance

- Technology and AI: The S&P 500's strong performance is driven by technology and AI stocks. Investing in these sectors could be promising, especially with the ongoing advancements in AI and machine learning.

- Mining and Resources: The ASX 200 has significant exposure to mining and resources, which can be attractive if commodity prices remain strong. Companies like BHP and Rio Tinto are key players in this sector.

Dividends Yields

Australian companies often offer higher dividend yields compared to their US counterparts. This can be appealing for income-focused investors looking for steady returns.

Valuation

The S&P 500 has seen significant gains and may be considered pricey by some investors. In contrast, the ASX 200 might offer better value, especially if the market corrects or stabilises.

Long-Term Growth

Historically, both indices have delivered respectable returns. The S&P 500 has shown higher average returns over the past few years, but the ASX 200 provides a more stable and consistent performance with dividends.

Risk Management

Investing in both markets can help spread risk. While the US market may offer higher growth potential, the Australian market provides stability and income through dividends.

In summary, investing in both the S&P 500 and the ASX 200 can be a strategic approach because it gives you a mix of different types of investments. The S&P 500 has lots of big tech companies that can grow quickly, while the ASX 200 has more stable companies that pay out regular dividends.

By putting your money in both markets, you spread out your risk. This means if one market doesn't do well, the other might still perform okay, helping balance things out.

This combination of investments can give you a good mix of growth potential and steady income. It helps you to balance making money now and growing your investment for the future.

The Residential Property Market

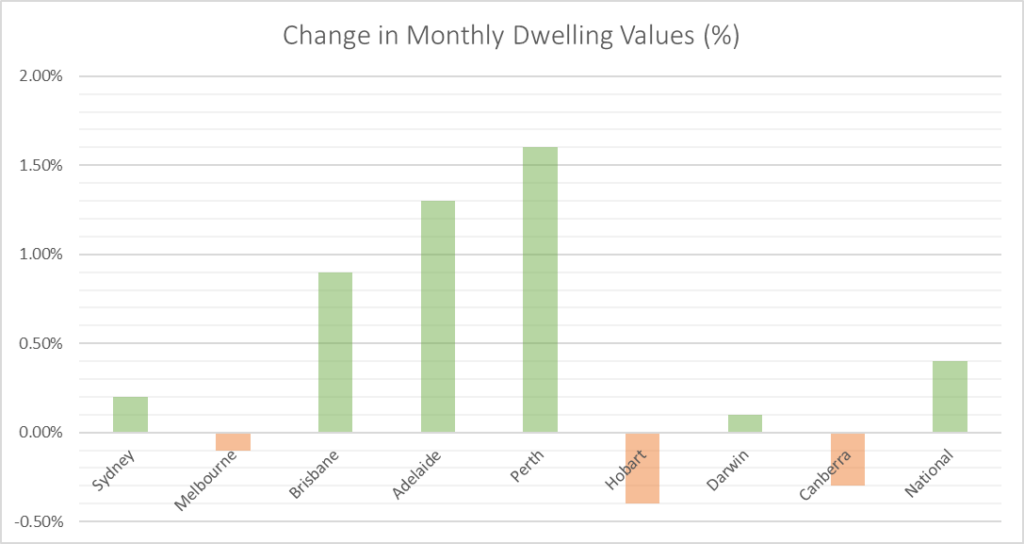

The Australian residential property market showed a varied landscape as we moved through September and October 2024, with national dwelling values inching up by a modest 0.4% in September. This growth, while positive, indicates a slowing momentum compared to earlier in the year. Let’s explore some of the noteworthy points highlighted in the October 2024 CoreLogic HVI report.

Capital Cities

- Perth led the pack with a robust 4.7% increase over the September quarter, with a monthly rise of 1.6%.

- Adelaide followed closely, recording a 4.0% rise for the quarter and a 1.3% increase in the month.

- Brisbane showed steady growth at 2.7% for the quarter, with a 0.9% monthly gain.

- Sydney's growth slowed to 0.5% for the quarter, its lowest since early 2023, with a modest 0.2% monthly increase.

- Melbourne experienced a decline of 1.1% over the quarter, the most significant drop among capital cities, and saw a 0.1% decrease for the month.

On the other hand, growth in regional housing markets also eased, with the combined regionals index showing a 1.0% increase over the September quarter, down from 1.7% in the June quarter.

A significant milestone was reached this month, with the total value of residential real estate hitting $11 trillion. This represents a substantial increase from $10 trillion just 15 months earlier, highlighting the rapid growth in property values despite recent slowdowns.

Market Dynamics

Several factors contributed to the changing landscape of the property market:

- More Properties for Sale: The number of new properties listed for sale was 3.2% higher than the previous year. This increase in available homes could give buyers more options to choose from.

- Affordability Issues: Less expensive properties continued to perform better than pricier ones. The value of homes in the lower price range increased by 12.4% over the past year, while more expensive properties only saw a 3.8% increase.

- Slower Rental Market: The national rental index only increased by 0.1% over the September quarter, which is the smallest change in four years. This suggests that rent prices are not rising as quickly as they were before.

- Longer Selling Times: Homes are taking longer to sell, with the average time on the market increasing to 32 days in the September quarter, up from 29 days in the previous quarter.

Looking Ahead

The outlook for the Australian property market remains positive, with several factors at play:

- Potential Interest Rate Cuts: There's a possibility that interest rates might be reduced either late this year or early next. If this happens, it could make borrowing money easier and boost confidence in the property market.

- Ongoing Housing Supply Challenges: There are continuing difficulties in building new homes due to issues like tight profit margins for builders and a shortage of tradespeople. This ongoing lack of new housing could help keep property prices and rents from falling too much.

- Affordability Concerns: Despite the potential for interest rate cuts, housing affordability remains a significant issue. The amount of household income needed to pay a new mortgage was at record highs in June, making it difficult for many people to buy homes.

- Credit Availability: There's a chance that getting loans might become more difficult. The Reserve Bank of Australia is keeping a close eye on how much debt households are taking on, which could lead to stricter lending standards.

- Population Growth: Australia's population is expected to reach 27 million by 2025, potentially adding pressure to housing demand.

As we move towards the end of 2024, the Australian residential property market is characterised by slowing growth and increasing diversity across regions. While some areas continue to see significant gains, others are experiencing modest declines. Buyers may find more opportunities with increased listings, but affordability remains a key concern. The market's future trajectory will likely be influenced by interest rate decisions, supply constraints, and broader economic factors.

Inflation and Interest Rates

The RBA kept the cash rate target at 4.35% during its September meeting. This was the seventh time in a row that they decided not to change interest rates since they last increased them in November 2023. This shows that the RBA is being careful about how they manage the economy.

Inflation Concerns

The RBA is still worried about inflation, which is the general increase in prices over time. They specifically mentioned that the "trimmed mean measure of inflation" remains too high for comfort.

To explain this in simpler terms, the trimmed mean measure of inflation is a special way of calculating price increases. Imagine you have a list of price changes for different items. Instead of using all of them, you remove the most extreme changes (both the biggest increases and the biggest decreases) and then take the average of what's left. This gives a more stable picture of inflation by ignoring unusual price swings.

The RBA uses this method because it helps them see the overall trend in prices without being distracted by temporary or extreme price changes in specific items.

Labour Market

The employment situation in Australia is strong. In September, a record high percentage of Australians were either working or actively looking for work. Over 64,100 people found new jobs that month, with most of these being full-time positions. The unemployment rate stayed at 4.1%, which is considered low.

Consumer Spending

The RBA expects people to spend more in the second half of 2024. However, they think this increase might be slower than they originally thought. This could mean that people are being careful with their money due to uncertainty about the economy.

Future Outlook

The RBA is keeping a close eye on things that could cause inflation to rise further. They plan to keep their current policy of high interest rates for some time. This approach is designed to help bring inflation back to their target range of 2-3%.

Different banks have varying predictions about when interest rates might start to decrease. Most are suggesting that gradual reductions might begin sometime in 2025. While the banks agree on the peak rate of 4.35%, they differ in their predictions of how quickly and by how much the rate will decrease. However, the strong labour market data has made it less likely that there will be a rate cut before the end of 2024.

Market Impact

The continued high interest rates and uncertain economic outlook are creating challenges for property investors and homeowners. This situation could potentially affect the real estate market and make renting more expensive for some people.