Newsletter – September 2024

The Share Market

This month turned out to be a surprisingly positive month for share markets, defying the usual "September effect" that often sees stocks struggle. Both the Australian S&P/ASX 200 and the US S&P 500 managed to climb higher, giving investors a reason to smile.

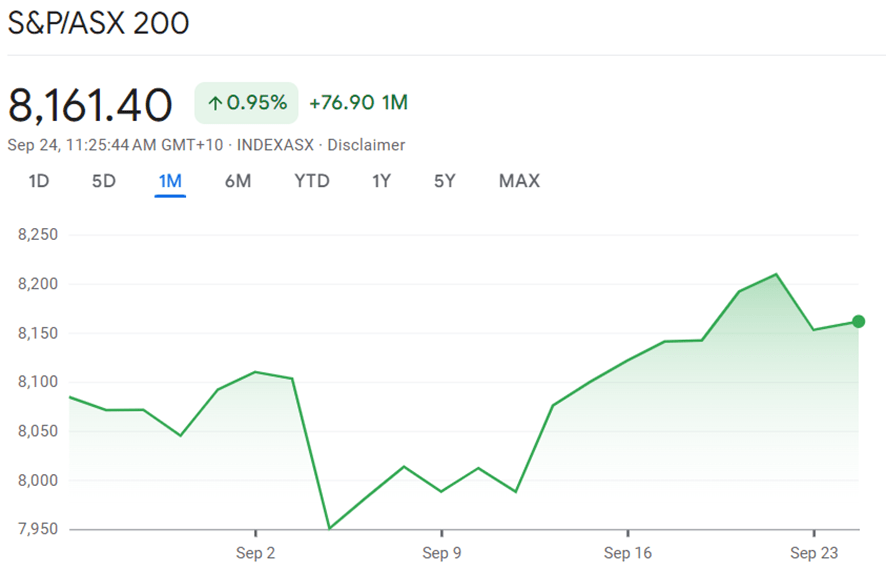

The ASX 200 had quite a journey this month. It started September on shaky ground, dipping down to around 7,925 points early in the month. However, it then steadily climbed its way up. By the end of the month, it had reached a respectable 8,161.40 points, marking a 0.95% increase. This performance is particularly noteworthy given September's historical reputation as a challenging month for stocks. Even more impressively, the ASX 200 reached new all-time highs. The index hit a record high of 8,199.6 points on September 19, 2024.

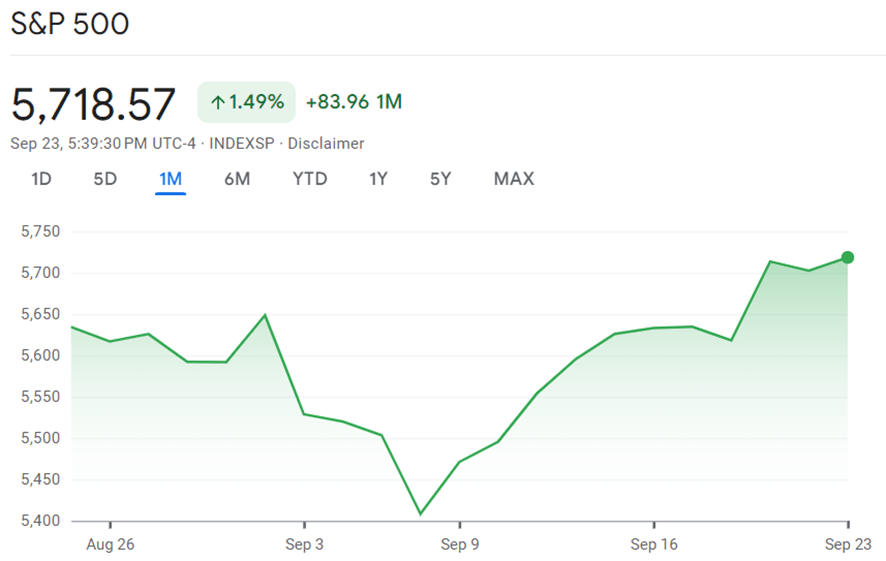

Over in the US, the S&P 500 put on an even more impressive show. It rose by 1.49%, finishing the month at 5,718.57 points. But it wasn't all smooth sailing - the index took a bit of a tumble earlier in the month, nearly touching 5,400 points before bouncing back. This recovery demonstrates the underlying strength of the US market, despite some initial volatility.

So, what was behind this unexpected September surge? Several key factors came into play:

Interest Rate Cut

The big news was the US Federal Reserve's decision to cut interest rates by 50 basis points, bringing them down to the 4.75%-5.00% range. This was the first rate cut since March 2020, and it sent ripples of excitement through the markets. Investors tend to react positively to lower interest rates as they make borrowing cheaper and can stimulate economic growth. This decision had a significant impact not just on US markets, but on global markets as well, including Australia.

Strong Jobs Data

Australia's job market showed remarkable strength in August 2024. According to the Australian Bureau of Statistics (ABS), the country added around 47,000 jobs in August, well above market expectations. This strong employment growth helped keep the unemployment rate steady at 4.2%, which is historically low. The participation rate remained at its record high of 67.1%, indicating that a large proportion of the working-age population is actively engaged in the labor market. This robust jobs data contributed to positive market sentiment and helped support the ASX 200's upward trajectory.

Mining Sector Boost

The ASX 200 got a significant boost from the mining sector. Uranium and lithium miners saw some big gains, partly thanks to geopolitical factors and increased demand. For example, Russia's Vladimir Putin threatened to limit uranium exports as retaliation to Western sanctions, which led to huge gains for uranium miners. Similarly, lithium miners traded higher due to increased demand from China's electric vehicle production. This sector-specific strength added to the overall positive performance of the ASX 200.

Real Estate Rally

The real estate sector in Australia had a particularly good gain. This impressive gain was likely due to speculation about interest rate cuts and the actual Fed decision. Real estate investment trusts (REITs) are typically sensitive to interest rate changes, and the prospect of lower rates often leads to increased investor interest in this sector. We will discuss more on real estate, specifically residential property market, in the next section.

Global Market Optimism

The positive performance wasn't limited to Australia and the US. Europe's broader market index, the STOXX 600, neared its all-time high, benefiting from the positive sentiment surrounding the Fed's rate cut decision. In Asia, Hong Kong's Hang Seng index rose above the 18,000-point mark for the first time in 2 months, and Japan's Nikkei 225 rose by 2.10% despite a weakening yen. This global market optimism contributed to the overall positive trend in September.

In a market like this, how should investors best approach it? This is where Modern Portfolio Theory (MPT) comes in handy. MPT, developed by Harry Markowitz in the 1950s, suggests that investors shouldn't put all their eggs in one basket. Instead, it's smart to spread investments across different types of assets, based on your risk apetite. This is also more commonly known as diversification.

In a market where we saw growth in various sectors, MPT would suggest creating a diverse portfolio. This might include:

- Stocks from different sectors (e.g., mining, real estate, technology)

- Bonds, which can provide stability when stocks are volatile

- International investments to take advantage of global trends

- Alternative investments like commodities or real estate investment trusts (REITs)

The idea behind MPT is that by spreading investments, you're less likely to get badly hurt if one particular area of the market takes a dive. It's about balancing risk and return across your entire portfolio, rather than trying to pick individual winning stocks.

For example, an investor might allocate a portion of their portfolio to ASX 200 stocks to capitalise on the strong performance of the Australian market, while also investing in US stocks to benefit from the S&P 500's growth. They might also include some bonds for stability, and perhaps some exposure to the booming real estate sector through REITs.

However, it's important to note that while MPT provides a framework for diversification, it doesn't eliminate all risk. Market conditions can change rapidly, and past performance doesn't guarantee future results. The strong performance we saw this month might not continue indefinitely, and investors should always be prepared for market fluctuations.

Remember, while this month was a good month for stocks, the market can be unpredictable. It's always a good idea to keep an eye on your investments, stay informed about market trends and economic indicators, and adjust your strategy as needed. Consulting with our team of trusted advisers can also be helpful in creating a diversified portfolio that aligns with your individual financial goals and risk tolerance. As always in the world of investing, it's important to approach the market with a well-thought-out strategy and a long-term perspective.

The Residential Property Market

Australia's housing market continues to show resilience and growth, with national dwelling values rising 0.5%. This marks the 19th consecutive month of increase, according to the latest CoreLogic Home Value Index (HVI) report. However, the pace of growth is moderating, with the quarterly increase in national home values (1.3%) now less than half the rate observed in the same period last year. Let’s explore the national overview, capital city specifics, regional markets, and other noteworthy points highlighted in the September 2024 CoreLogic HVI report.

National Overview

The national housing market is experiencing sustained growth, with dwelling values up 0.5% in August. This brings the total annual growth to 7.1%, with the national Home Value Index now at a record high. However, the pace of growth is slowing, with the quarterly increase of 1.3% being significantly lower than the 2.7% observed in the same period last year.

The moderation in growth can be attributed to a more balanced flow of supply and demand. While there's still more demand for housing than available supply overall, the situation varies markedly between regions.

Capital City Specifics

Capital cities are showing diverse growth patterns:

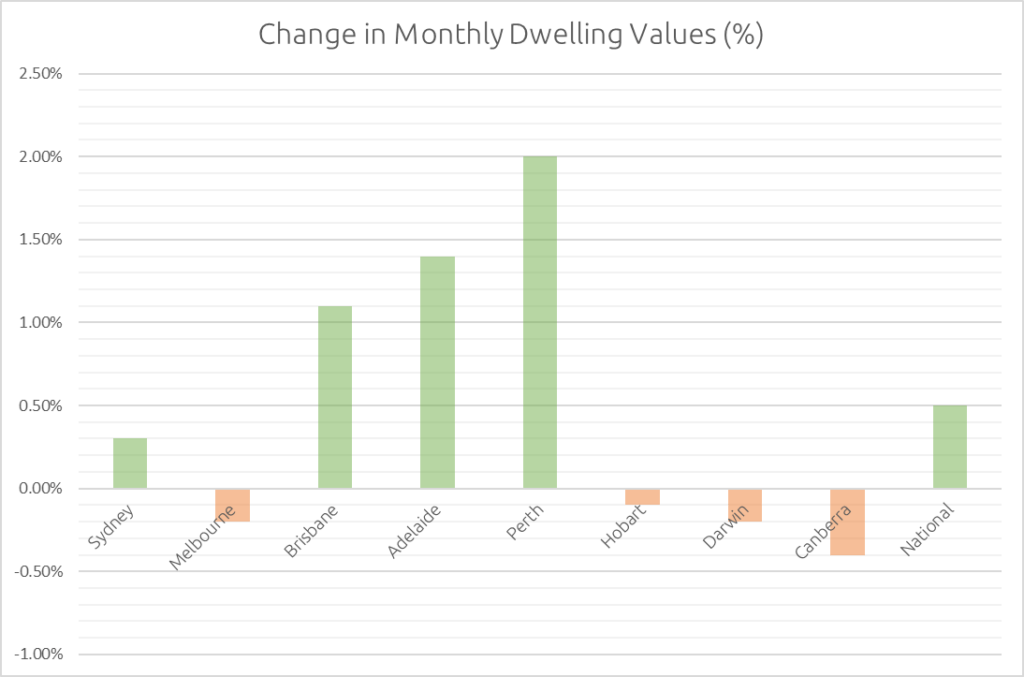

- Perth leads with a strong monthly gain of 2.0%, followed by Adelaide at 1.4% and Brisbane at 1.1%.

- Sydney's growth has slowed to a mild 0.3% for the month.

- Four capital cities experienced declines: Canberra (-0.4%), Melbourne (-0.2%), Darwin (-0.2%), and Hobart (-0.1%).

Notably, Melbourne's median dwelling value has been overtaken by both Adelaide and Perth, making it the third lowest among capital cities. Adelaide's median now stands at $790,800, and Perth's at $785,250, compared to Melbourne's $776,044.

Regional Markets

Regional markets are underperforming compared to their capital city counterparts. The combined regional markets saw a modest 1.1% rise in dwelling values over the quarter, less than half the rate of combined capitals.

This softer performance appears to be demand-driven, with estimated home sales in regional areas 6.5% lower than a year ago. However, many regional markets still have low levels of advertised supply, which is helping to maintain some upward pressure on prices.

Rental Market

The rental market remains tight, with vacancy rates at record lows: 1.0% across capital cities and 1.2% in regional areas. However, the pace of rental growth is easing in most markets. The combined capitals saw a quarterly rise in rents of 1.9% in August, down from 2.7% in June.

The easing in rental growth can be attributed to several factors. Rising costs have created affordability issues, which in turn have led to a trend towards larger households, ultimately reducing overall rental demand. Additionally, there has been a decrease in net overseas migration, further contributing to the slowdown. This may bring the end of the rental boom closer.

Affordability Concerns

While rising home values benefit homeowners, affordability constraints are worsening for non-homeowners. The ratio of dwelling values to household income has reached 7.4, and the portion of household income needed to service a new mortgage is approaching record highs at 45.5%.

Future Outlook

The housing market outlook remains positive but could slow further. Key factors to watch include advertised supply levels, consumer sentiment, interest rates, and lending conditions. The ongoing undersupply of housing, coupled with strong population growth, is likely to support housing values over the medium term.

Australia's residential property market continues its recovery, with national values reaching new highs. However, growth is moderating, and regional disparities persist. Affordability remains a significant concern, particularly in the rental market, as the country grapples with housing undersupply amid strong population growth.

Inflation and Interest Rates

The Reserve Bank of Australia (RBA) has announced its decision to keep the cash rate target unchanged at 4.35% during its September 24, 2024 meeting. This marks the seventh consecutive meeting where the central bank has maintained the current interest rate.

Inflation Concerns

The RBA noted that inflation remains above the target range of 2-3% and is proving persistent. While inflation has fallen substantially since its peak in 2022, it is still some way above the midpoint of the target range. The central bank does not expect inflation to return sustainably to target until 2026.

Economic Outlook

The board emphasised that the economic outlook remains highly uncertain. Factors contributing to this uncertainty include:

- Softening outlook for the Chinese economy

- Geopolitical uncertainties

- Mixed signals from other central banks globally

Market Reaction and Expectations

The decision to hold rates steady was largely anticipated by economists and market analysts. Prior to the announcement, a survey of 45 economists had predicted that the RBA would maintain its key interest rate unchanged.

Implications for Borrowers

The decision to hold rates means that borrowers will not face an immediate increase in their loan repayments. However, the RBA's commitment to bringing inflation down suggests that rates may remain elevated for some time. Having said that, a hold is still much more welcoming news than an increase in rates for borrowers.

Future Outlook

The RBA emphasised that it will continue to rely on incoming data and evolving assessments of risks to guide its future decisions. Key areas of focus will include:

- Developments in the global economy and financial markets

- Trends in domestic demand

- Inflation outlook

- Labor market conditions

The board remains open to all options, stating that it is "not ruling anything in or out" regarding future policy decisions.

In conclusion, while the RBA has maintained its current stance, it continues to balance the need to control inflation with supporting economic growth and employment.