Newsletter – May 2025

The Share Market

Both the ASX 200 and S&P 500 delivered impressive gains throughout May 2025, with each index posting solid monthly returns that reflected growing investor confidence across Pacific markets. The Australian benchmark achieved a steady 5.13% increase, while the US market outperformed with a 7.10% gain, though this came with notably higher volatility. These movements occurred against a backdrop of improving economic conditions, including inflation moving within target ranges and renewed consumer confidence following trade developments.

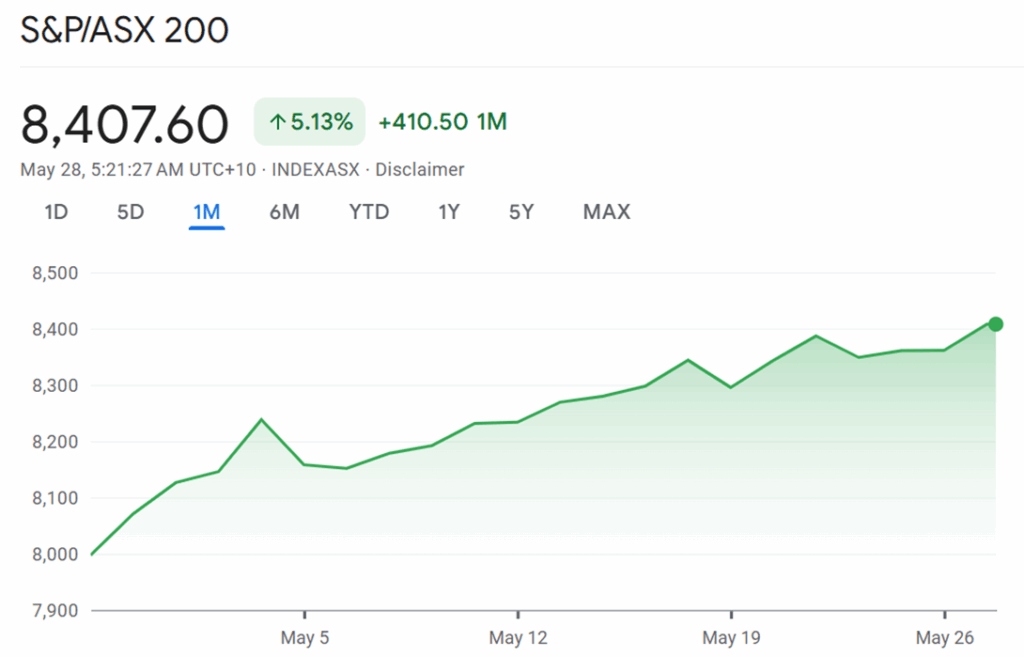

ASX 200 Delivers Consistent Growth Through May

The S&P/ASX 200 Index demonstrated remarkable consistency throughout May, climbing from approximately 8,000 points at the month's beginning to close at 8,407.60 points, representing a gain of 410.50 points or 5.13%. The index's trajectory was characterised by steady upward momentum with relatively minor fluctuations, suggesting sustained investor confidence in Australian equities.

Source: Google Finance

The month began with the index hovering just above the 8,000-point threshold, from where it embarked on a measured ascent. Early May saw consistent gains that pushed the benchmark towards 8,200 points by around May 5th. A brief consolidation period followed, with the index experiencing a modest pullback before resuming its upward path. This pattern of growth followed by short-term consolidation repeated throughout the month, creating a staircase-like progression that ultimately led to the strong May close.

The index's performance accelerated during the final week of May, with a particularly strong finish that brought it to its highest point for the month. This late surge coincided with improved market sentiment following the Reserve Bank of Australia's decision to lower the cash rate target to 3.85% at its May meeting. The RBA's move was driven by inflation settling within the 2-3% target range, providing additional support for equity markets.

Sector performance during May was broadly positive, with financials and industrials leading the charge. Financial stocks benefited from the changing interest rate environment and reduced political uncertainty, while industrial companies gained from safe-haven demand and improved business conditions. Notable performers included Commonwealth Bank, which reached new yearly highs with a 64.9% annual gain, and Brambles, which achieved a remarkable 100.7% yearly increase.

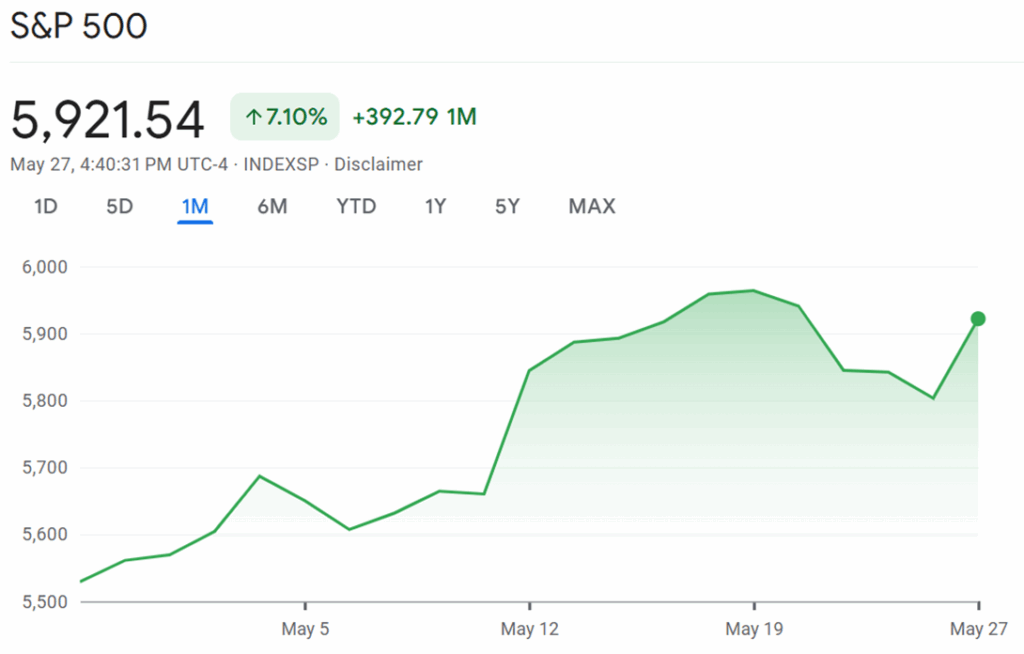

S&P 500 Posts Higher Gains Amid Greater Volatility

The S&P 500 Index delivered a stronger percentage gain than its Australian counterpart, rising 7.10% or 392.79 points to close at 5,921.54 points by May 27th. However, this superior performance came with significantly more volatility, as the index navigated various economic crosscurrents and policy developments throughout the month.

Source: Google Finance

The US benchmark began May around 5,540 points and initially followed a similar trajectory to the ASX 200, with steady early gains pushing the index towards 5,700 points by early May. The first notable acceleration occurred around May 10-12, when the index surged dramatically to approach 5,900 points. This sharp rise coincided with improving corporate earnings, with S&P 500 companies reporting a blended year-over-year growth rate of 13.6% in the first quarter of 2025.

The index reached its monthly peak around May 19th, touching levels near 5,950 points before experiencing a notable correction. This pullback saw the index retreat to approximately 5,800 points, highlighting the increased volatility that characterised the US market during this period. The decline was partly attributed to ongoing concerns about tariffs and their potential economic impact, which remained at the forefront of consumer sentiment.

However, the S&P 500 demonstrated remarkable resilience in the final trading sessions of May, staging a strong recovery that brought it close to the month's highs. This late-month surge was supported by improving consumer confidence, which increased by 12.3 points in May to 98.0, marking a significant rebound after five consecutive months of decline. The recovery in confidence was broad-based across age groups and income levels, providing additional support for equity markets.

The continued strength of technology stocks, particularly artificial intelligence-related companies, played a significant role in the S&P 500's performance. The 'Magnificent Seven' technology giants continued to drive market gains, with investors remaining optimistic about AI sector prospects. This technological focus helped differentiate the US market from other global indices and contributed to its outperformance relative to international peers.

Economic Factors Supporting Market Performance

Both markets benefited from improving macroeconomic conditions during May. In Australia, the RBA's monetary policy adjustment reflected growing confidence that inflation pressures were moderating while economic growth remained supported. The central bank noted that inflation was now within the target range as higher interest rates had successfully slowed demand in some economic sectors.

Meanwhile, US economic data showed strengthening fundamentals, with corporate profits rising substantially and GDP growth forecasts being revised upward. UBS recently increased its year-end S&P 500 projection to 6,000 points, citing earnings that exceeded expectations and enhanced economic growth prospects. The health care sector experienced particularly strong growth of 43%, while communication services and information technology sectors also contributed significantly to overall market gains.

Consumer confidence improvements in the US provided additional support for equity markets. The Conference Board's Consumer Confidence Index showed that consumers became less pessimistic about business conditions and employment prospects over the next six months. Importantly, consumers' outlook on stock prices improved markedly, with 44% expecting stock prices to increase over the next 12 months, up from 37.6% in April.

Understanding Momentum in Market Movements

The sustained upward trends observed in both the ASX 200 and S&P 500 during May can be understood through the lens of momentum investing theory. Momentum investing is a strategy that capitalises on the continuance of existing market trends, based on the principle that securities showing upward price movement tend to continue rising for extended periods. This approach suggests that once a trend becomes well-established, it is likely to persist, which helps explain why both indices maintained their positive trajectories throughout most of May.

The behaviour observed in May demonstrates classic momentum characteristics, where investors tend to buy securities that are already rising and sell those that are declining. This creates a self-reinforcing cycle where positive price movements attract more buyers, further driving prices higher. The ASX 200's steady climb and the S&P 500's strong recovery after mid-month volatility both illustrate how momentum can sustain market trends, even in the face of short-term uncertainties. Professional momentum investors focus on technical indicators rather than fundamental analysis, seeking to identify and ride these trends for as long as they persist.

However, it’s important to note that momentum investing isn’t without its risks. Trends can reverse suddenly, especially if market sentiment shifts or unexpected news emerges. This can lead to sharp losses if investors are caught on the wrong side of a move. Additionally, momentum strategies can sometimes encourage buying at already high prices, which increases the risk of a downturn. Because of these pitfalls, it’s wise to approach momentum investing with caution and consider seeking professional financial advice to ensure your investment approach matches your personal goals and risk tolerance.

Conclusion

May 2025 proved to be a rewarding month for investors in both Australian and US equity markets, though each index exhibited distinct characteristics. The ASX 200's steady 5.13% gain reflected confidence in Australia's economic stability and the supportive monetary policy environment. The index's consistent upward trajectory suggested that domestic investors maintained a positive outlook throughout the month, supported by strong performance across key sectors including financials and industrials.

The S&P 500's higher 7.10% return came with the trade-off of increased volatility, as the index navigated various economic and policy uncertainties. Despite short-term fluctuations, the underlying strength of corporate earnings and technological innovation provided a solid foundation for continued gains. Both markets finished May on a positive note, with momentum carrying into the final trading sessions and setting an optimistic tone for the months ahead.

The performance of these two major indices during May highlights the resilience of developed market equities in the face of ongoing global uncertainties. With inflation pressures moderating, corporate earnings growing strongly, and consumer confidence recovering, both the ASX 200 and S&P 500 appear well-positioned to continue their positive trajectories, though investors should remain mindful of the different risk-return profiles each market presents.

The Residential Property Market

The Australian residential property market demonstrated sustained upward momentum through April and May 2025, even amidst a climate of economic and political unpredictability. Data recently released from CoreLogic’s Home Value Index (HVI) paints a picture of nuanced trends across both capital city and regional housing markets, influenced by shifts in interest rates, sentiment surrounding the federal election, and persistent constraints on housing supply.

National Trends Indicate Record Highs

Nationally, the Home Value Index recorded a 0.3% ascent in April. This rise signified the third consecutive month of growth, successfully propelling Australian dwelling values to a new record high. In tangible terms, this monthly increase translated to an average gain of approximately $2,720 in the median value of an Australian home. Encouragingly, all capital cities contributed to this positive trajectory by posting increases in property values. However, despite this overall growth, the pace observed in April was somewhat more subdued than the 0.4% increase seen in March. This moderation is thought to reflect a softer consumer sentiment and lower auction clearance rates, as both buyers and sellers exhibited a degree of caution leading up to the federal election and in response to newly announced US tariffs.

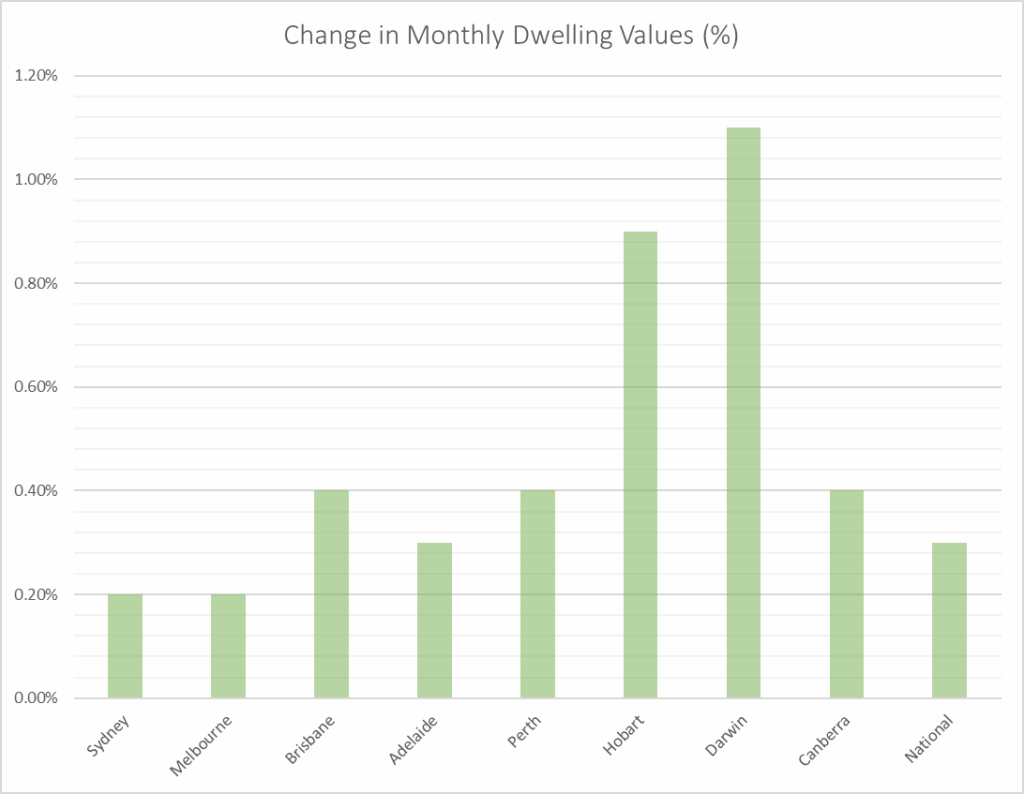

Source: CoreLogic’s Home Value Index (HVI) May 2025

Capital City Performance

Across the nation's capitals, April saw a universal rise in dwelling values, though the extent of this growth varied. Darwin led the charge with a notable 1.1% increase. Australia's largest cities,

Sydney and Melbourne, both experienced more modest monthly gains of 0.2%. Brisbane and Perth also saw values climb by 0.4%, while Adelaide recorded a 0.3% rise. Hobart saw a significant 0.9% jump, and Canberra values were up by 0.4%.

Despite these recent gains, not all markets have fully recovered to their previous peak values. For instance, Sydney's dwelling values still sit 1.1% below their high point recorded in September 2024. Melbourne's market shows an even wider gap, with values remaining 5.4% beneath their 2022 peak. When viewed annually, the national growth rate slowed to 3.2% in April, marking its lowest point since August 2023 and indicating a loss of the stronger momentum witnessed in late 2024 and early 2025.

Regional Markets

Regional Australia, in particular, demonstrated considerable strength, with property values increasing by 0.6% in April. This performance outpaced the combined capital cities, which saw a lesser 0.2% rise. The regional markets of South Australia and Western Australia were standout performers, recording the strongest monthly gains at 1.5% and 1.3% respectively. This trend, where regional markets grow faster than their capital city counterparts – a pattern prominent during the COVID-19 pandemic – appears to have re-emerged since October 2024, suggesting a renewed appeal for housing outside the major metropolitan hubs.

Houses vs Units

The preference for detached houses over units continued to influence value changes. House values generally appreciated at a faster rate than units, a trend particularly evident in Sydney. Over the quarter, Sydney houses gained 1.4% in value, while unit values in the Harbour City experienced a slight decline of 0.3%. Hobart presented a similar divergence, with houses up by 1.4% over the quarter, contrasting with a 1.1% fall in unit values. Conversely, the unit sectors in Brisbane and Perth showed stronger growth dynamics compared to houses in those cities during the same period.

Rental Market Growth Moderates

In the rental market, the pace of growth has begun to moderate. The national rental index saw a seasonally adjusted rise of 0.4% in April. More significantly, annual rental growth has slowed considerably, dropping from a high of 8.3% in April 2024 to 3.6% in April 2025. While Perth continues to lead the nation in annual rental growth at 5.7%, this is a substantial decrease from the 13.6% recorded a year prior. Sydney and Melbourne have seen their annual rental growth slow to 1.9% and 2.0% respectively. Despite this easing, national gross rental yields reached a two-year high of 3.73%, with regional yields even more attractive at 4.41%, indicating that rental income as a proportion of property value has improved.

Key Market Drivers and Future Outlook

Several factors influenced market dynamics during the April-May period. While the February rate cut had provided an initial boost to housing conditions, its positive effects had begun to diminish. However, the Reserve Bank of Australia's decision last week to implement another cash rate reduction is expected to inject renewed confidence into the market. This move, widely anticipated and now realised, is likely to further stimulate buyer interest and activity, potentially counteracting some of the recent hesitancy linked to tariff announcements and pre-election uncertainty.

Despite this monetary policy easing, listing volumes and auction activity through April and early May reached their lowest levels for this time of year since 2019. This subdued activity was partly attributed to the timing of public holidays and the typical slowdown observed during a federal election campaign.

Housing affordability remains a significant structural challenge across Australia. The national dwelling value to household income ratio persists at record levels (8.0), and mortgage serviceability, even prior to the latest rate cut, was at an all-time high, with median-income households dedicating a substantial portion of their gross income to repayments. While the recent rate cut will offer some relief on borrowing costs and improve serviceability calculations for new and existing mortgage holders, the underlying affordability pressure from high property values remains.

Population growth has largely normalised from the sharp fluctuations seen post-pandemic. Nevertheless, a persistent undersupply of housing continues to provide a fundamental support for property values. This imbalance, now coupled with lower borrowing costs following the RBA's recent action and the expected increase in certainty post-election, is anticipated to underpin modest value growth for the remainder of 2025. The market will be watching closely to see how quickly lenders pass on the rate cut and the extent to which it translates into increased borrowing capacity and demand.

Influence of Policy and Supply Constraints

Housing policy has been a key focus for both major political parties, with various stimulatory measures proposed. These include expanded deposit guarantee schemes and potential tax changes, primarily aimed at assisting first home buyers in entering the market. However, the supply side of the housing equation continues to face significant hurdles. New dwelling commencements remain well below the decade average, and construction costs continue their upward trajectory, further exacerbating the existing supply constraints and making the delivery of new housing stock more challenging.

The overall market outlook remains finely balanced. Positive influences, such as lower interest rates and policy stimulus, are contending with significant challenges including stretched affordability, cautious lending practices by financial institutions, and generally subdued consumer sentiment.

Conclusion

In summary, the Australian residential property market has demonstrated notable resilience through April and May 2025, navigating economic and political headwinds to achieve new record high values. Regional markets and the detached housing sector have generally outperformed capital cities and units, while the rapid escalation in rental growth has eased. As the year progresses, the interplay between anticipated interest rate movements, the impact of government policy stimulus, and the persistent issue of housing supply will be pivotal in shaping the market's direction. A period of modest further growth is generally anticipated as market certainty returns post-election and monetary policy settings remain supportive.

Inflation and Interest Rates

Australia’s economic landscape in May 2025 is marked by a welcome moderation in inflation and a notable shift in interest rate policy, as both households and businesses adjust to a changing global and domestic environment.

After several years of elevated price pressures, inflation in Australia has eased considerably. According to the Australian Bureau of Statistics, the Consumer Price Index (CPI) rose by 2.4% over the twelve months to the March 2025 quarter, matching the pace seen at the end of 2024 and representing a four-year low. This marks the first sustained period since late 2021 where both headline and core (trimmed mean) inflation have returned to the Reserve Bank of Australia’s (RBA) 2–3% target range. The moderation is most evident in the services sector, where cost increases have slowed sharply, and overall, the data indicate that inflationary pressures are now more balanced.

While housing, education, and food prices posted notable increases in the March quarter, these were partially offset by declines in recreation, culture, and household goods. The RBA expects inflation to remain stable around the midpoint of its target range, though a temporary uptick is anticipated when certain cost-of-living support measures expire later in the year.

Reflecting the improved inflation outlook, the RBA cut its cash rate by 25 basis points at its May meeting, lowering it from 4.10% to 3.85% — the lowest level in two years. This is the first rate cut since January and comes after a prolonged period of steady rates. The central bank’s decision was in line with market expectations and aimed at supporting economic growth amid global uncertainties and subdued domestic demand.

The RBA Board cited the return of inflation to target and a more balanced risk profile as reasons for the move, but also noted that the global backdrop remains volatile, especially with ongoing trade tensions and weaker external demand. The Board emphasised its readiness to act if international developments threaten domestic stability.

Australian lenders have responded to the RBA’s rate cut, with major banks such as NAB, ANZ, Commonwealth Bank, and Westpac announcing reductions in their standard variable home loan rates, effective from late May and early June. However, not all banks have passed on the full cut, prompting scrutiny from consumer advocates and policymakers. For many mortgage holders, the reduction offers some relief after a period of higher borrowing costs.

Despite the positive inflation news, the outlook for Australia’s economy is tinged with caution. The RBA expects GDP growth to pick up only gradually, as global headwinds and slower household spending weigh on momentum. The unemployment rate remains low at around 4.1%, but is projected to edge up slightly, stabilising below 4.5% — still favourable by historical standards.

Consumer inflation expectations remain elevated at 4.1%, reflecting ongoing concerns about cost-of-living pressures, even as actual inflation has moderated. The RBA and government continue to monitor these dynamics closely, balancing the need for price stability with support for growth. In summary, May 2025 finds Australia in a period of relative stability on the inflation front, with the RBA taking its first steps towards easing monetary policy. While the environment remains uncertain, especially given global developments, the current trajectory offers cautious optimism for households, businesses, and policymakers alike.