Newsletter – July 2025

The Share Market

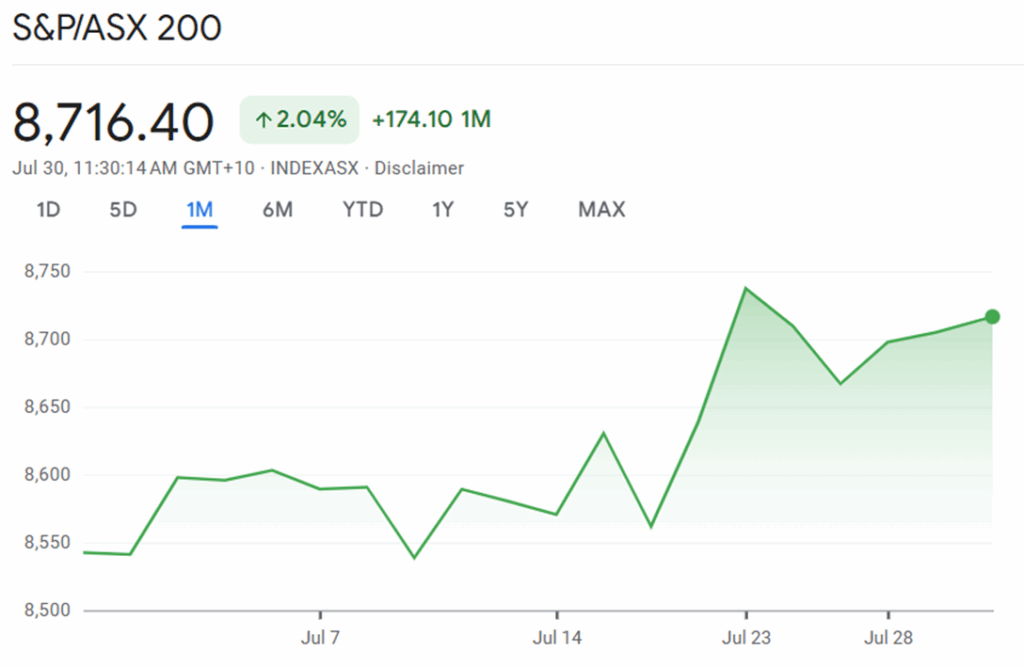

ASX 200 Performance

July has been a month of measured optimism for the Australian share market. The S&P/ASX 200 index, which tracks the Australian stock exchange’s top 200 companies, wrapped up the month at 8,716.40, reflecting a 2.04% rise and gaining 174.10 points over the last 30 days.

Source: Google Finance

At the start of July, the ASX 200 sat just above the 8,550 mark. Early movements in the month were modest yet positive, with the index drifting past the 8,600 mark within the first few trading sessions. This initial lift was likely underpinned by continuing strength in the resources sector, steadfast consumer spending, and a general mood of stability from statements made by the Reserve Bank.

The upward trend encountered some turbulence in the first half of the month. Around July 10–14, the index slipped below 8,600, momentarily approaching the 8,550 level — the lowest point for July. However, this dip was temporary, and the market quickly rebounded. Such movements frequently occur in response to a combination of global developments and local news, including earnings updates and changing investor sentiment.

Around this time, Australia was feeling the effects of mixed signals from China, its largest trading partner. Questions surrounding trade relations, particularly the ongoing US-China tariff talks, contributed to market volatility. In addition, lingering concerns over global inflation kept investors somewhat cautious, as did the sector rotations prompted by new earnings guidance from major companies.

During the latter part of July, the index saw a more consistent and significant rise. Notably, around July 23, the ASX 200 surged toward 8,740, marking its monthly high. Although there was a slight pull-back thereafter, the index finished strongly as the month drew to a close.

This robust performance was probably buoyed by strong quarterly results from key Australian companies, especially in the mining sector, and positive remarks from the central bank. Global sentiment also played its part, with improved outlooks helping to reinforce investor confidence despite ongoing international uncertainties.

While the month wasn’t without its swings, the overall picture for the ASX 200 in July was one of resilience and cautious progress. The market dealt with external pressures, navigated fluctuations, and managed to close the month on a positive note.

S&P 500 Performance

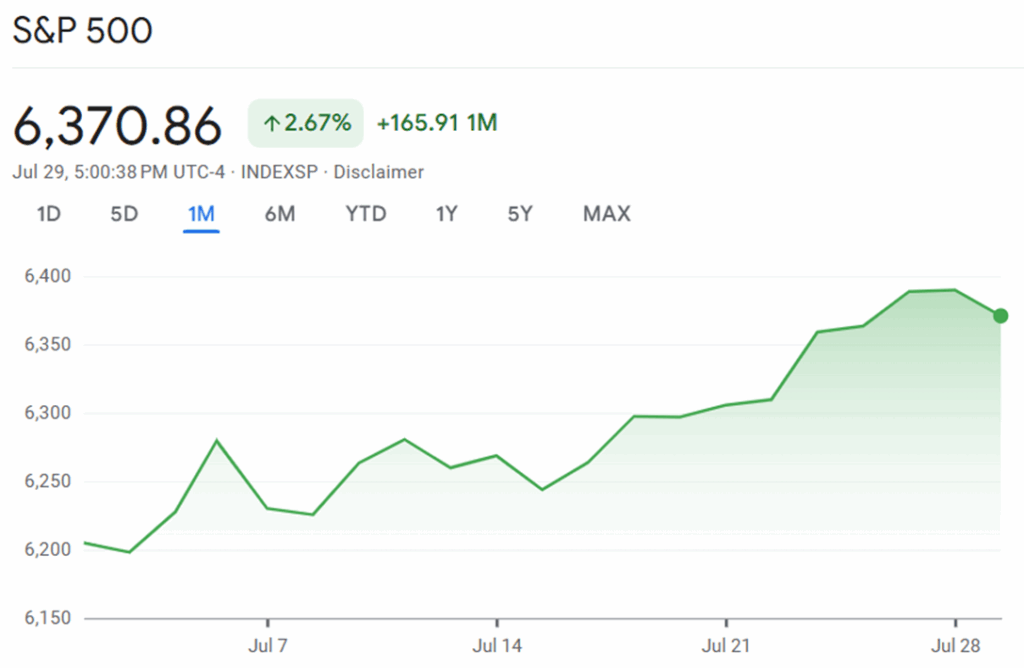

Looking overseas, the S&P 500 index, which covers the largest American companies, posted even more impressive gains through July. By the end of the month, the S&P 500 stood at 6,370.86, rising by 2.67% and gaining 165.91 points since the start of the month.

Source: Google Finance

The first days of July saw the S&P 500 sitting just above 6,200, with the index gradually climbing higher. This movement was notably steady, punctuated by a sharp push upwards around July 5–7, when the index neared 6,300. Strong performances from the technology sector helped boost confidence, as did a general sense of optimism following recent communications from the US Federal Reserve.

The middle of the month introduced some volatility, with the index vacillating within the 6,250–6,300 range. Economic data emerging at the time — including jobs reports, inflation figures, and updates on consumer confidence — were closely watched by market participants. Speculation grew regarding the Federal Reserve’s upcoming rate announcement, with investors weighing the prospect of an interest rate cut in the near future. Quarterly earnings reports from major technology and consumer companies also moved the market, contributing to the short-term jaggedness in the chart.

A pronounced rally characterised the last stretch of July, as the S&P 500 advanced past 6,350 by around July 25. The strong run was fuelled by encouraging quarterly results from large corporations, especially in the technology sector, as well as signs that the US economy was coping with higher interest rates without slipping into recession. Despite a brief retreat in the final sessions of the month, the S&P 500 ended July firmly in positive territory.

Global concerns were never far from investors’ minds, particularly as the ongoing discussions between the US and China over tariffs continued to create an undercurrent of uncertainty. Attention sharpened as the market looked ahead to the impending Federal Reserve rate announcement, which was highly anticipated by market watchers seeking signals about future monetary policy.

Key Takeaways

In summary, July proved to be a constructive month for both the ASX 200 and the S&P 500, though the US market edged ahead in gains percentage-wise.

The ASX 200’s performance tells a story of resilience under pressure, finishing the month with a late rally that affirmed confidence in the Australian market.

The S&P 500, meanwhile, offered consistent growth and a stronger recovery, underpinned by robust corporate earnings, an economy that continued to defy pessimistic forecasts, and hope for supportive signals from the Fed.

All of this unfolded against the backdrop of ongoing international uncertainty, with global trade issues — particularly those stemming from the US-China tariff negotiations — continuing to cast a long shadow. As the world’s eyes await the Fed’s next move, both markets seem poised, if cautious, heading into August.

The Residential Property Market

Data recently released from Cotality's Home Value Index (HVI) reveals a renewed sense of optimism in the Australian residential property market through June and July 2025. This latest snapshot captures the impact of multiple Reserve Bank rate cuts, the tempo of housing value recovery, and ongoing shifts in city and regional trends. Below is a detailed update grounded in Cotality’s June HVI, supported by additional reliable sources.

National Highlights: Steady Growth Amid Rate Cuts

Australian housing values climbed by 0.6% in June 2025, marking the fifth consecutive month of growth following a brief downturn late last year. This upturn has lifted the national median dwelling value to $837,586 as of 30th June, with cumulative growth of 2.4% over the first half of 2025.

Two rate cuts—first in February, then May—acted as clear catalysts, reversing the earlier slump and fuelling a broad-based surge in housing sentiment. The Reserve Bank of Australia opted to keep the official cash rate steady in July, pausing to gauge the effects of these recent reductions while signalling a cautious outlook in a still-uncertain economic climate. Tim Lawless, research director at Cotality, noted that “growing certainty of more cuts later in the year have further fuelled positive housing sentiment, pushing values higher”. Financial markets are now tipping the official cash rate to drop to about 3.1% by December, with some speculation it could go even lower.

The current recovery, however, is more moderate than previous surges. The 1.4% quarterly growth rate is measured when contrasted to the frenzied 3.3% quarterly peak of mid-2023, and remains positively tepid compared to the pandemic-era highs of 8.1% quarterly growth.

Supply and Demand

Despite rising values, turnover remains subdued. Housing turnover in the first half of 2025 sits at an annualised 4.9%, slightly below the decade average of 5.1%, reflecting continued hesitancy among sellers and persistent affordability constraints.

Advertised supply is limited — stock levels are 5.8% lower than this time last year and down 16.7% against the previous five-year average. The interplay of mild demand (just below average) and tight supply has resulted in a relatively balanced market for buyers and sellers, buttressed by a lift in auction clearance rates, now hovering above the decade average in the mid-60% range.

City-by-City Review

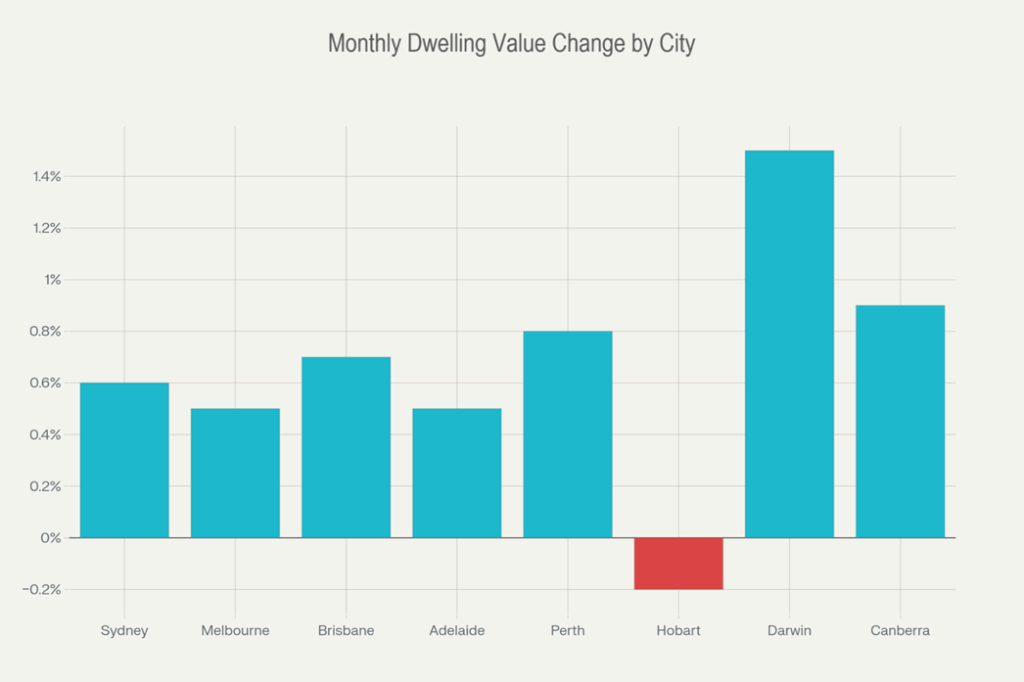

The June data showcase significant regional variation. Nearly every capital and rest-of-state region posted gains in June, apart from Hobart (-0.2%). Below is a breakdown of the monthly changes for Australia’s major cities:

Source: Data from Cotality

- Sydney: +0.6%. As Australia’s most expensive housing market, Sydney saw a continued upward tick, bringing its median value to $1,210,222 by the end of June.

- Melbourne: +0.5%. Melbourne’s market, after a prolonged underperformance, has regained balance, registering four consecutive months of growth with a median value at $796,952.

- Brisbane: +0.7%. With strong population growth and tight supply, Brisbane notched another solid monthly rise, its five-year gains now topping 75%.

- Adelaide: +0.5%. Still among the most robust cities, propelled by short supply and consistent buyer demand, Adelaide’s annual growth hit 8.0% with a median of $837,176.

- Perth: +0.8%. Outpacing other capitals in both monthly and annual growth, Perth’s market continues to benefit from interstate migration and subdued construction pipelines, reaching a median of $819,885.

- Hobart: -0.2%. Hobart was the only capital to see a monthly slip, continuing a softening trend since its 2022 peak.

- Darwin: +1.5%. Darwin led quarter-on-quarter growth (4.9%), pushing its dwelling values to a new record high, and finally surpassing its previous peak from 2014.

- Canberra: +0.9%. Canberra’s market revived after a slow patch, though growth is now more restrained.

Regional Australia: Growth Accelerates

While the combined capitals captured much of the spotlight, regional markets showed resilience. The combined regional index rose 0.5% in June, and 1.6% over the quarter — outpacing capitals for quarterly growth. Standout areas include parts of regional Queensland and Western Australia where major resource and agricultural regions have driven double-digit annual price increases. For example, Mid West in regional WA and Darling Downs (West) - Maranoa in QLD saw annual gains over 20%.

Rental Market and Yields: Growth Slows, Yields Stabilise

National rental growth has eased, with rents rising 1.3% through Q2 — the lowest quarterly rise since 2020 as vacancy rates remain tight (average just above 1%). Annual rental index growth slid to 3.4%, a significant move down from the highs of 8% to 10% during the post-pandemic demand surge. Gross rental yields have steadied: across major capitals, yields now range from 3.1% in Sydney up to 6.5% in Darwin, with regional markets typically yielding more than city centres.

“Hobart and Darwin have seen a strong acceleration in annual rental growth, topping the annual change leader board for both houses and units,” Cotality’s report notes.

Lending, Affordability, and Regulation: Challenges Remain

While the market’s tailwinds — lower rates, high confidence, tight labour markets, and low supply — are supporting price growth, there are clear hurdles ahead. Affordability remains a key constraint: the median Australian household is now spending roughly one-third of pre-tax income on rent or mortgage repayments. High household debt (over 180% of disposable income) and cautious lending policies temper the potential for another period of rapid price inflation.

The number of loans issued to borrowers with debt-to-income ratios exceeding six times has been below 6% since mid-2023, suggesting that lending standards remain prudent. Regulatory agencies note any future surge in credit could prompt tighter rules.

Outlook: Modest Upswing Expected

Looking forward, the consensus among major analysts is that house values are on track to outpace the long-term annual average, with projections indicating a 5.8% rise nationally by the end of 2025 — above the average rate of 5.2% per year. Further rate cuts are expected to buoy buyer sentiment and support values, but ongoing affordability issues and weak income growth are likely to temper the extent of gains.

In summary, Cotality’s latest HVI paints a picture of an Australian housing market entering a new phase: one defined by gentler price acceleration, sturdy market confidence, and persistent supply challenges. The balance of 2025 should see values edge higher, but with all eyes remaining on interest rates, household incomes, and the pace of economic recovery.

Inflation and Interest Rates

Inflation: Stable Within Target

Australia’s inflation eased further in July 2025, confirming a trend of moderation that’s been underway since late 2024. Official figures from the Australian Bureau of Statistics show that annual inflation for the June quarter was 2.1%, lower than the 2.4% recorded in March and marking the lowest level since 2021. This places inflation comfortably within the Reserve Bank of Australia’s (RBA) official target band of 2–3%.

The most significant price increases over the quarter were in housing, education, and food, though these were partially offset by dips in recreation and household goods. Trimmed mean inflation — a key measure used by the RBA — dropped as well, alongside falling petrol prices in late July after having spiked temporarily earlier in the month due to international events.

Interest Rates: RBA Holds Steady after Earlier Cuts

In its July meeting, the RBA Board opted to hold the cash rate steady at 3.85%, slightly defying many market expectations for another rate cut. This follows cuts in February and May, totalling a 50 basis points reduction since the start of 2025.

The RBA’s minutes show a balanced debate: a majority felt continuing with a “cautious and predictable” approach was warranted, given inflation remained within the target and the jobs market was still relatively tight. A minority, meanwhile, highlighted possible downside risks and argued for further cuts, but there was no call for any large adjustment. Market consensus currently expects another reduction in August or November, but the central bank has flagged ongoing uncertainty — particularly around global trade and energy prices — which could affect future decisions.

What’s Behind the Trends?

Several factors have been steering both inflation and interest rates this year:

- Cooling price pressures, especially for fuel, have helped bring overall inflation down.

- Previous rate increases are still making their way through the economy, keeping domestic demand subdued.

- The labour market remains tight, but wage growth’s rise has slowed, partly limiting further inflation.

- Global events, especially brief spikes in oil prices from mid-year conflicts, added volatility but didn’t create a lasting surge in cost-of-living pressures.

Looking Forward

Most economists and Australia’s major banks predict that the cash rate will head lower by the end of 2025 — likely settling between 3.1% and 3.35%. Future central bank moves will depend on inflation remaining within target and no major shocks to jobs or global markets. For now, Australians are experiencing a period of relative stability, with both inflation and interest rates in 2025 staying well within recent historical norms. While the RBA remains ready to act if conditions change, July’s decisions suggest a preference for steady, watchful management over dramatic policy shifts.