Newsletter – February 2025

The Share Market

Australia – ASX 200

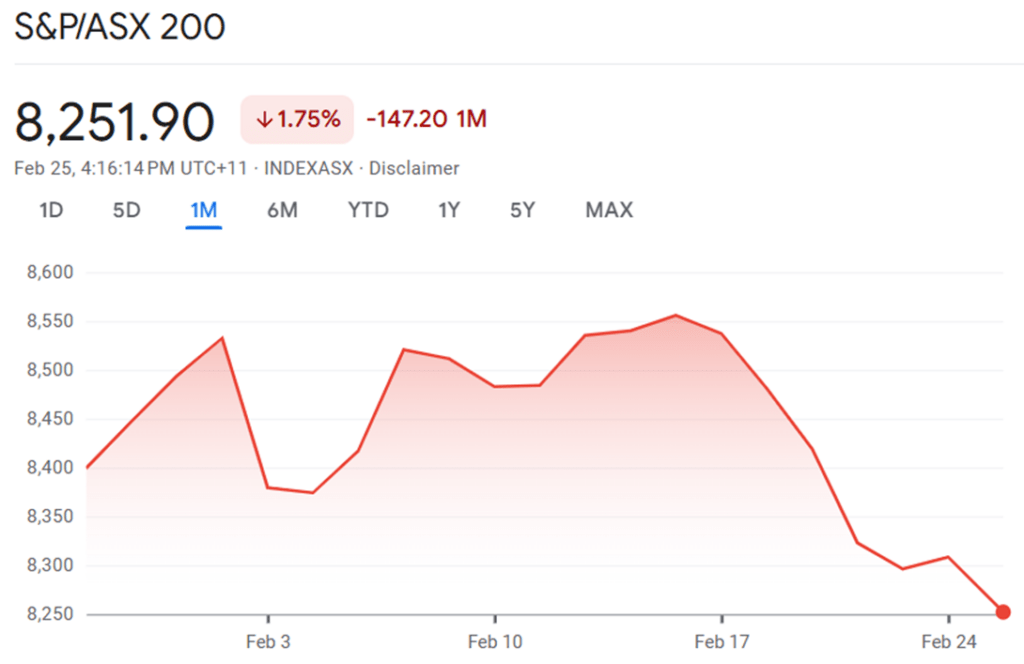

The S&P/ASX 200, Australia's benchmark stock index, has experienced a turbulent February, with the index currently sitting at 8,251.90 as of 25 February 2025. This represents a decline of 1.75% or 147.20 points over the past month, reflecting a challenging period for Australian equities.

The ASX 200 began the month on a positive note, climbing from around 8,400 on 3 February to reach a peak of approximately 8,550 by 5 February. However, this optimism was short-lived, as the index experienced a sharp drop to about 8,350 by 7 February.

In a display of resilience, the market rallied once more, touching another high of roughly 8,550 on 12 February. Unfortunately, this second peak marked the beginning of a gradual decline that has persisted through the latter half of the month.

Several factors have contributed to the ASX 200's lacklustre performance in February:

- Global Tech Jitters: The local market has been influenced by nervousness on Wall Street, particularly in the tech sector. Investors have been cautious ahead of Nvidia's highly anticipated earnings report.

- Disappointing Earnings: The Australian earnings season has delivered some high-profile disappointments, weighing on investor sentiment. For instance, AMP Ltd, an ASX 200 financial stock, saw its shares plummet by 22.9% this month following poor full-year results.

- International Trade Concerns: US President Donald Trump's announcement of new tariffs on Mexico and Canada, set to commence next month, has added to market pressures.

- Banking Sector Weakness: Key players in the banking sector, including Westpac, Bendigo Bank, and NAB, have provided disappointing trading updates, contributing to a broader weakness in financials.

- Commodity Price Pressures: Lithium and coal stocks have continued to struggle due to weak commodity prices and operational challenges.

The market's performance has varied significantly across different sectors:

- Financials: Despite recent struggles, some financial stocks like Hub24 and Netwealth Group have seen substantial gains over the past year.

- Industrials: Companies like Brambles have reached 52-week highs, buoyed by strong earnings and improved guidance.

- Materials: This sector has faced challenges, with companies like Mineral Resources experiencing significant share price declines due to operational issues and increased capital expenditure forecasts.

While the ASX 200 has faced headwinds in February, it's worth noting that the index remains up 1.57% since the beginning of 2025. Analysts at Trading Economics expect the index to trade at 8,428 points by the end of the first quarter of 2025, suggesting some potential for recovery in the near term.

USA – S&P 500

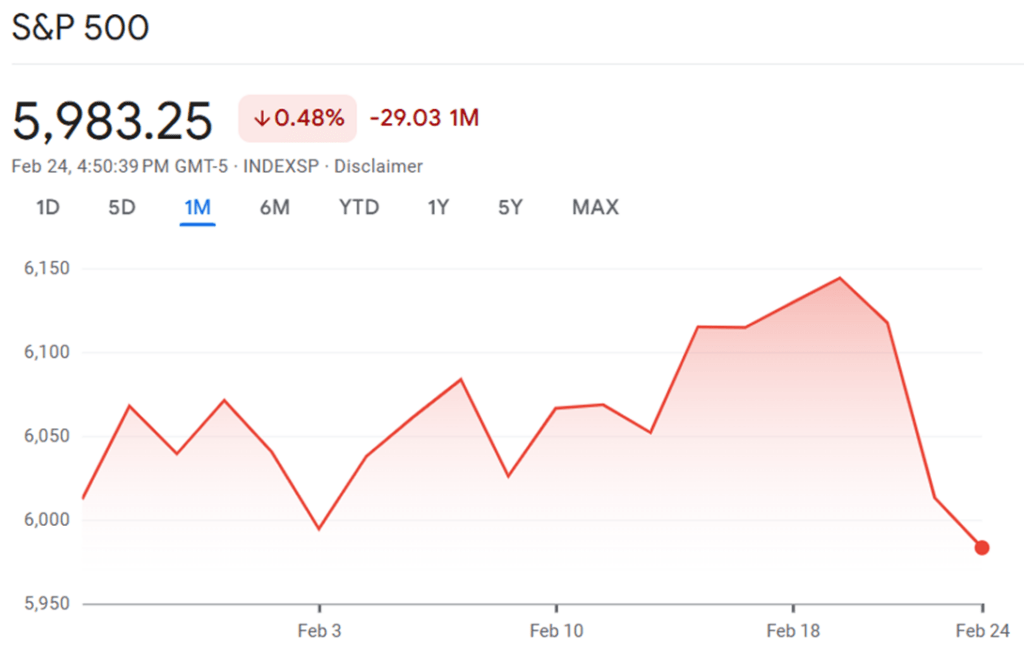

The S&P 500, America's benchmark stock index, has experienced a volatile February, with the index currently standing at 5,983 as of 24 February 2025. This represents a modest decline of 0.48% or 29.03 points over the past month, reflecting a challenging period for US equities.

The S&P 500 kicked off the month near the 6,000 mark and quickly gained momentum, reaching a peak of approximately 6,050 by 3 February. However, this initial optimism was short-lived, as the index experienced a dip to around 6,000 by 10 February.

Showing resilience, the market rallied once more, touching a new high of roughly 6,100 on 18 February. Unfortunately, this second peak marked the beginning of a decline that has persisted through the latter half of the month, bringing the index down to its current level of 5,983.

Several factors have contributed to the S&P 500's choppy performance in February:

- Economic Data Concerns: Fresh economic data has raised worries about the health of the US economy, leading to increased market volatility.

- Trade Tensions: President Donald Trump's new tariff plans have dented investor confidence, adding pressure to the market.

- Sector Performance Variations: Different sectors have shown varied performance, with some, like healthcare, showing strength while others, such as consumer discretionary, have faced significant challenges.

- Tech Sector Pressure: Major technology companies have come under pressure, contributing to the Nasdaq's decline and potentially influencing the broader market.

- Earnings Season Impact: The ongoing earnings season has produced mixed results, with some high-profile disappointments affecting market sentiment.

The market's performance has varied significantly across different sectors:

- Healthcare: Showed strength with a 1.03% gain.

- Financials: Demonstrated resilience with a 0.67% increase.

- Consumer Discretionary: Faced significant challenges, declining by 0.47%.

- Technology: Experienced a slight dip of 0.38%.

As we approach the end of February, several key events could shape the market's direction:

- Nvidia Earnings: The market is eagerly anticipating Nvidia's earnings report, scheduled for release on 28 February, which could significantly impact tech sector sentiment.

- Fed's Inflation Report: The Federal Reserve's preferred inflation gauge, set to be released on Friday, could influence expectations about future monetary policy.

- US Q4 GDP Revision: Thursday's revision of the fourth-quarter GDP figures may provide further insights into the economy's health.

While the S&P 500 has faced headwinds in February, it's worth noting that the index remains in positive territory for the year. However, investors should remain cautious given the ongoing global economic uncertainties and the mixed performance across different sectors of the US market.

As always, a diversified investment approach and careful consideration of individual company fundamentals remain vital in these challenging market conditions. With key economic data and earnings reports on the horizon, market participants will be closely watching for signs of both the S&P 500’s and ASX200's directions in the coming weeks.

The Residential Property Market

The Australian residential property market has started 2025 with a mix of stability and subtle shifts, reflecting ongoing affordability challenges, economic uncertainty, and regional growth. Here’s a detailed look at the key updates from January to February 2025 based on the most recent CoreLogic report.

National Trends

- Dwelling Values: National home values remained largely stable in January, dipping slightly by 0.03%. This follows a year of strong growth in 2024, with the annual growth rate slowing to 4.3% in January 2025, down from 9.7% a year earlier.

- Capital Cities vs Regional Areas: Capital cities experienced a 0.2% decline in dwelling values, while regional markets outperformed with a 0.4% increase, reaching record highs. This trend highlights the continued appeal of regional areas due to affordability and lifestyle factors.

Capital City Performance

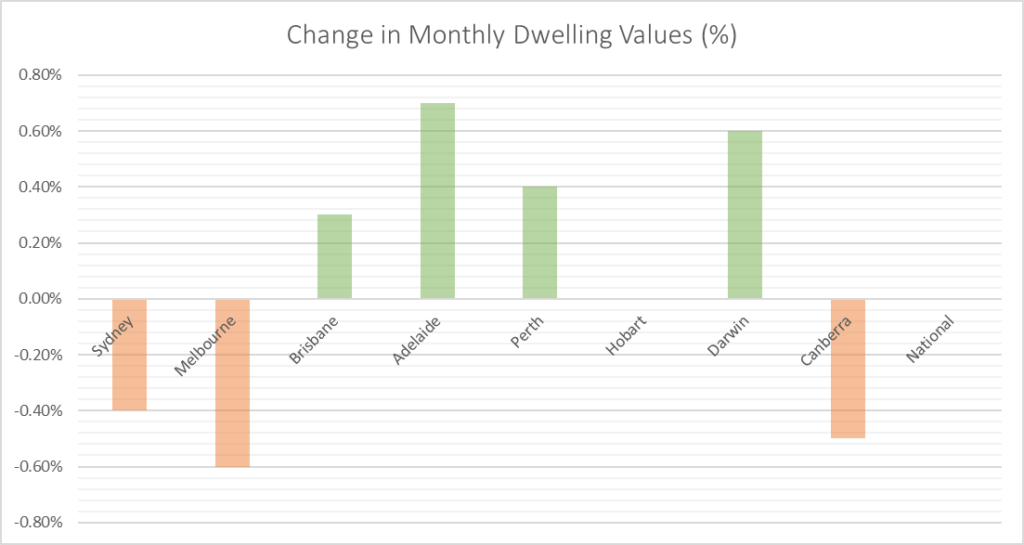

The performance across capital cities was uneven:

- Declines: Melbourne (-0.6%), Canberra (-0.5%), and Sydney (-0.4%) recorded the most significant drops in January.

- Growth: Brisbane and Perth continued to see price increases, although the pace of growth has slowed compared to previous months.

- Flat Markets: Hobart showed no change in dwelling values during January.

Regional Markets

Regional Australia continued to shine:

- Dwelling values rose by 0.4% in January, driven by increasing demand for affordable housing and lifestyle benefits outside major cities.

- Regional Victoria was the only regional market to see a decline (-0.15%) in January4.

Rental Market

The rental market remains tight:

- The average national rental asking price as of early February was $718 per week for houses and $557 for units.

- Affordability pressures continue to impact renters, with vacancy rates remaining low in many areas.

Property Listings

- Total property listings increased by 10.3% nationally in January, reaching 243,642 properties. Canberra led this rise with a 30.7% increase.

- The number of older listings (properties on the market for over 180 days) also rose by 7.2%, reflecting slower sales activity in some areas.

Market Drivers and Outlook

Several factors are shaping the property market:

- Interest Rates: The Reserve Bank of Australia's (RBA) decision on interest rates on February 18 (more on this in the following section) is expected to influence buyer confidence. A potential rate cut could boost borrowing capacity and drive price growth later in the year.

- Affordability Challenges: High property prices and limited income growth have strained affordability, particularly in capital cities.

- Regional Migration: Continued internal migration to regional areas is supporting demand outside metropolitan markets.

Predictions for 2025

Looking ahead:

- Many experts predict house prices will rise in 2025, driven by improving affordability, rising incomes, and potential further interest rate cuts.

- Brisbane, Perth, and Adelaide are expected to remain strong performers due to relative affordability and population growth.

In summary, while the national property market has stabilised early in 2025, regional areas are outperforming capital cities as buyers seek more affordable options. The outlook for the rest of the year will depend heavily on interest rate movements and broader economic conditions.

Inflation and Interest Rates

In a significant move, the Reserve Bank of Australia (RBA) has cut interest rates for the first time in over four years, reducing the cash rate from 4.35% to 4.10%. This decision, announced on 18 February 2025, marks a turning point in Australia's monetary policy and reflects the central bank's response to easing inflationary pressures.

The RBA's decision to cut rates comes after a prolonged period of restrictive monetary policy aimed at curbing inflation. The central bank's assessment suggests that some of the upside risks to inflation have eased, and disinflation might be occurring more quickly than previously expected. However, the RBA remains cautious, acknowledging that easing policy too much too soon could stall the disinflation process.

Governor Michele Bullock admitted that the RBA may not have raised interest rates quickly enough when inflation began to increase in mid-2021. This time, the RBA appears to be taking a more proactive approach, providing relief to borrowers before inflation definitively returns to the target band. This decision was made despite concerns about inflation and the strong Australian jobs market, which could drive wage growth and inflation.

The inflation outlook has improved significantly since late 2024. The Melbourne Institute's Inflation Gauge reported a 0.7% rise in underlying inflation for the December quarter. However, this marks a continued slowdown in inflationary pressures since March 2024, suggesting an environment that may support interest rate cuts.

However, the RBA staff's detailed economic analysis presented a more cautious view. Their report highlighted that the battle against inflation is far from over, suggesting a case for waiting for more concrete evidence before implementing rate cuts. The staff specifically noted the tightness of the labour market, the risk of firms pre-empting future productivity increases by demanding higher wages, and the possibility of wage growth moderating at a slower pace than desired.

The rate cut is expected to provide some relief to borrowers. All major banks will pass on the full 0.25% rate cut to variable home loan customers.

For savers, the outlook is mixed. While lower interest rates generally mean reduced returns on savings accounts, some banks are maintaining competitive rates on term deposits. CBA, for instance, is continuing its 10-month term deposit special at 4.60% p.a. for a limited time.

The rate cut is expected to stimulate economic activity by making borrowing more affordable. However, the RBA's approach remains cautious, with the central bank emphasising that monetary policy will remain restrictive even after this reduction. The aim is to achieve a more sustainable balance between demand in the economy and its overall capacity to supply goods and services.

While this rate cut marks a significant shift, economists are divided on the future path of interest rates. Some predict further cuts throughout 2025, with CBA forecasting a total reduction of 100 basis points over the year. However, other major banks, including ANZ and NAB, have pushed back their estimates for the next rate cut to May 2025. The coming months will be vital in determining whether this rate cut marks the beginning of a sustained easing cycle or a more measured approach to monetary policy adjustment.