Newsletter – April 2024

The Share Market

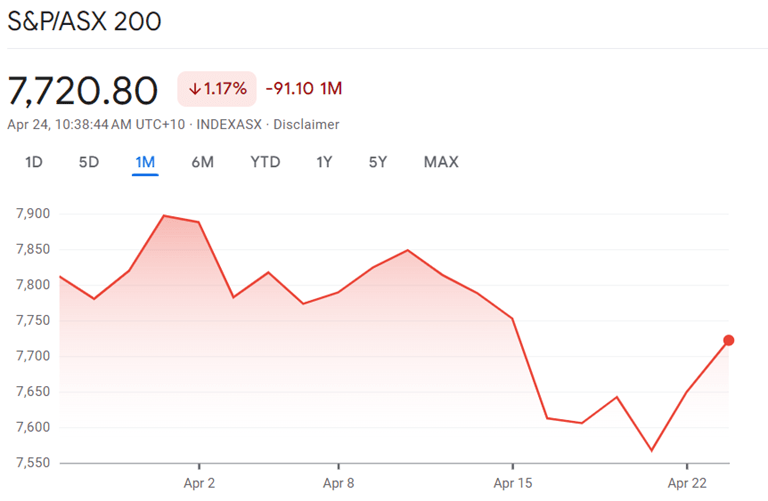

The ASX200, a bellwether for Australia's largest companies, experienced a modest decline of about 1.2% throughout April, ending slightly lower than where it started. This movement resembled a challenging bushwalk, with its ups and downs ultimately returning us near our starting point.

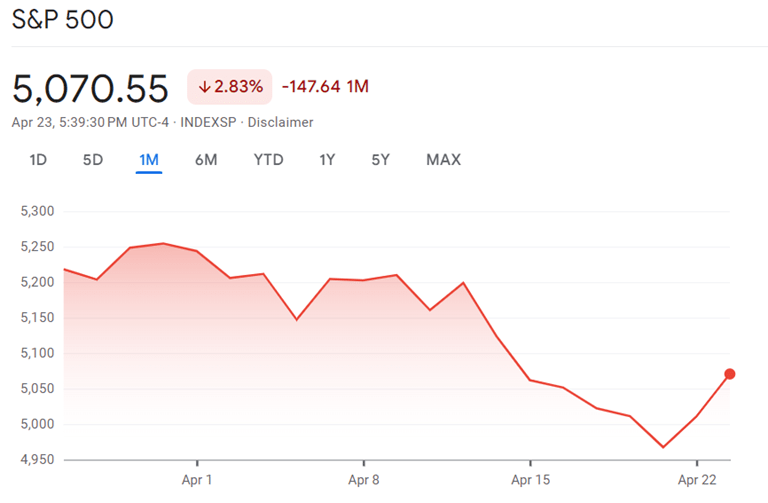

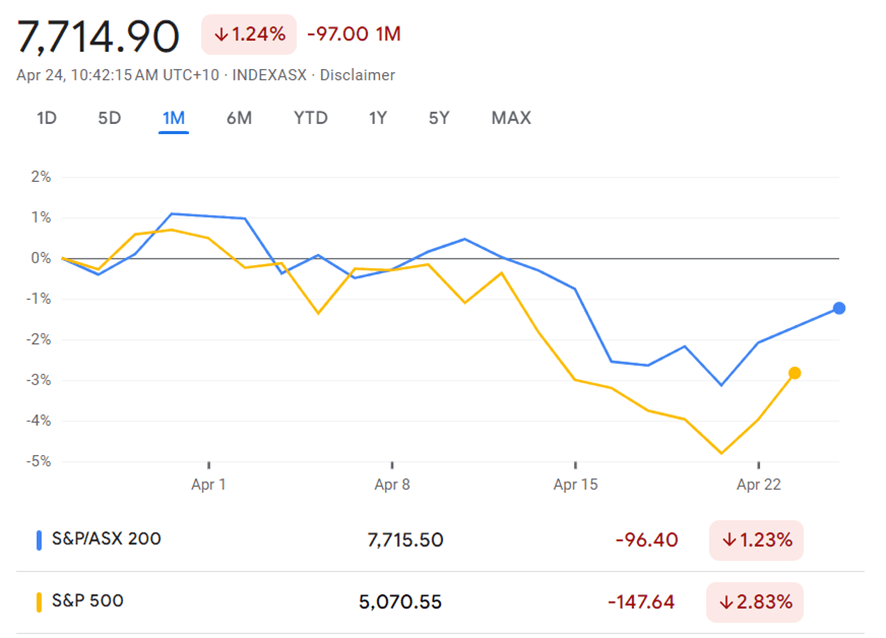

Internationally, the S&P 500 also demonstrated volatility, though with a sharper overall decline despite a late-month recovery. This comparison highlights the relative stability of Australian shares amidst global economic uncertainties.

A comparative look at the ASX200 and S&P 500 for April illustrates a stark contrast in stability. The Australian index demonstrated a steadier path through the month's economic volatility, declining by about 1.2%. This hints at a resilience that might be intrinsic to the Australian market amidst global economic headwinds. On the other side, the S&P 500 experienced a more substantial drop of 2.83%, perhaps reflecting a heightened sensitivity to the latest economic indicators, earnings reports, and geopolitical developments that have a pronounced impact on investor sentiment stateside. Let’s take a closer look.

During this period, the technology sector, particularly heavyweights such as Nvidia and major tech players like Netflix, Meta, Apple, and Microsoft, encountered notable downward pressures. As the period neared its end, technology stocks emerged as the underperforming segment of the S&P 500. There's a growing sentiment among investors that other market segments are yielding robust returns, which has led to a reallocation of investments, reducing exposure to the previously soaring tech stocks. This shift suggests a strategic trimming by investors looking to diversify and capitalise on the success of other industries. Investors pivot as more information becomes available.

One prevailing view of economic theories related to this is the Efficient Market Hypothesis. It suggests that the price of shares in the stock market includes everything that is known about those shares, like a soup that has all the ingredients mixed in. When new information pops up — like a company making more money than expected, the government changing tax rules, or if there's trouble in another country that affects global business — investors all over react to this news, and that reaction is seen in the rise or fall of stock prices. It's like a rumor spreading through a crowd, causing a buzz; the market's price moves because everyone's talking and making decisions based on the latest chatter.

One of the importances of this hypothesis is that it helps us understand why trying to outsmart the market, to guess when it will go up or down, is often a lost cause especially for the average investor. It tells us that all the known information about companies and the economy is already reflected in stock prices, so unless you have new information nobody else knows (which is unlikely and potentially illegal if it’s insider), you can't consistently predict market movements to make a quick profit. It supports the idea of long-term investing over trying to make quick, short-term gains by timing the market. This hypothesis is a big reason why many financial advisers suggest regular investing in a diverse set of stocks and steering clear of trying to time your buys and sells based on the day-to-day news.

April's share market activity serves as a practical example of the Efficient Market Hypothesis. Investors, upon hearing news from both home and abroad, made moves that were immediately reflected in the market. This could include anything from local economic reports, such as job numbers or policy changes by the government, to international events that have ripple effects all the way to our shores. Take, for instance, US crude oil prices edged lower after Iran recently said it will not escalate the conflict with Israel. This eased investor worries about inflation and interest rate decisions by the Federal Reserve. This intricate web of information and investor behaviour underscores the interconnected nature of global markets.

Understanding this hypothesis helps reinforce why many choose to invest consistently, regardless of daily market moves. For those with superannuation funds or personal investments in the share market, it's a reminder that staying the course is often more reliable than trying to guess which way the wind will blow next in the financial markets.

In essence, while the ASX200's and S&P500’s dips might prompt concern, they also illustrate the market's natural ebb and flow. This month's takeaway could be seen as a nudge for investors to focus on the long-term horizon, riding through the waves of volatility with a steady hand.

For the average investor, it's worth remembering that while the markets might have their rough days, the principles of regular, disciplined investing still stand. In the face of these downswings, keeping up with your investment strategy can pay off in the long run – it’s about consistency, not trying to time the market's every move.

While our analysis has focused on retrospective trends, it is important to note that such insights serve not as predictors, but as informative guides to better understand market dynamics. An informed investor is one who maintains a strategic approach, adapting to fluctuations without succumbing to the pitfalls of reactive decision-making.

We will continue to monitor market progressions, delivering insights that are both accessible and pertinent. We remain committed to equipping you with the knowledge to navigate the investment terrain with confidence and clarity.

The Residential Property Market

As we move further into 2024, the Australian housing market continues to demonstrate robust growth and resilience. March marked a significant point, with national home values celebrating a 14-month streak of consecutive increases. This upward trajectory in the housing sector reflects broader economic trends, making it an exciting time for investors and homeowners. Here's a deeper dive into the dynamics shaping the market, thanks to CoreLogic’s recent Home Value Index Report.

CoreLogic’s report reveals a continued rise in national home values, with a 0.6% increase over the last month alone. This growth adds approximately $112,000 to the median value over the March quarter, showcasing a strong recovery from the downturn experienced between April 2022 and January 2023. During that period, values dipped by 7.5%, but have since surged by 10.2%, adding about $72,000 to the median home value.

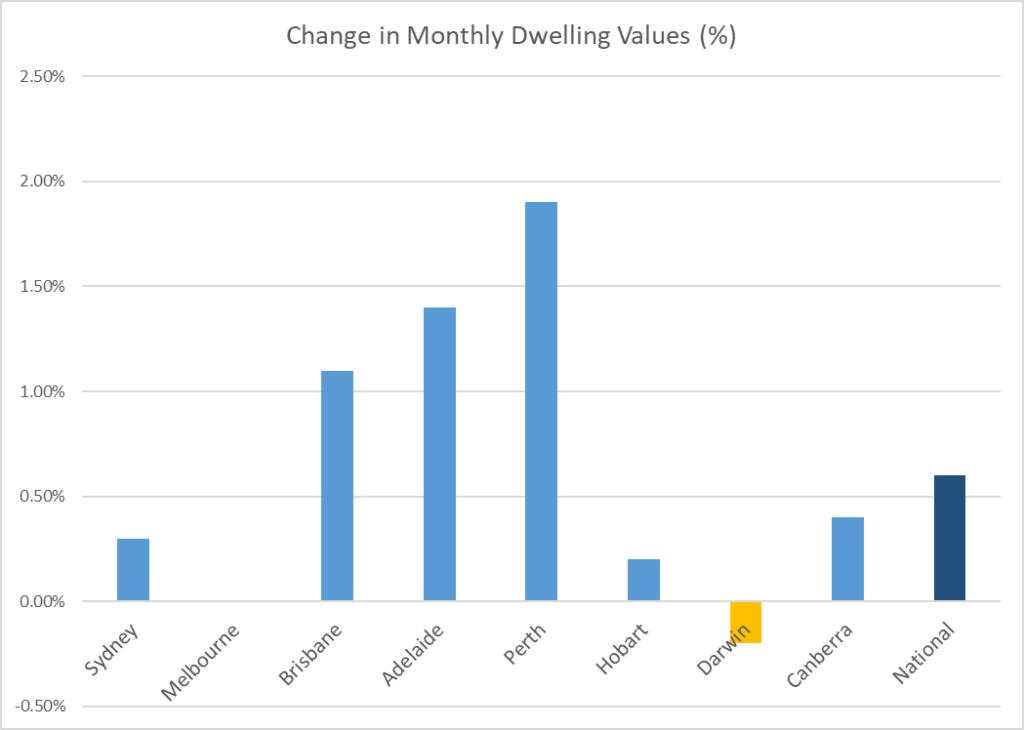

The market's resilience is also reflected in the diverse monthly performances across major cities:

- Perth leads with a notable 1.9% increase in home values over the month.

- Adelaide and Brisbane follow with increases of 1.4% and 1.1%, respectively.

- Melbourne remains unchanged, with a -0.2% change over the first quarter.

- Darwin saw a negative growth of -0.2% over the month.

This diversity is a clear indicator of varying local economic conditions, affordability issues, and differing levels of supply and demand.

The pace of growth has accelerated from 1.4% in the last quarter of the previous year to 1.6% in the first quarter of this year. However, it's important to note that the current quarterly growth rate is half of what was observed in the middle of last year, indicating a stabilisation in the rate of increase. This suggests that while growth continues, it is at a more sustainable pace, possibly due to the market adjusting to various economic pressures.

Interestingly, the strongest growth has now shifted to the lower quartile, or the least expensive 25% of homes, across most capital city markets. Put simply, the more affordable segment of the housing market is seeing the fastest growth in prices. This shift is largely driven by the increasing challenges around housing affordability and a decrease in borrowing capacity. The demand is now skewed towards the middle to lower end of the value spectrum, where properties are more accessible to a broader range of buyers.

Similar trends of diversity and growth are seen in regional markets, with Regional Victoria experiencing the softest growth conditions, notably down by 0.3% in the first quarter. Despite these varied conditions, the overall demand for housing remains strong. Home sales in the first quarter were estimated to be 9.5% higher relative to the same period last year, although this comparison starts from a relatively low base due to the previous downturn.

Looking ahead, the outlook for housing values remains positive. There is a growing expectation that interest rates will begin to fall later this year, which could further boost borrowing capacity and enhance consumer sentiment. However, the market continues to navigate challenges such as supply shortages, labor constraints, and the rising cost of materials.

Despite these hurdles, the fundamentals of housing supply and demand remain out of balance in most regions, placing continuous upward pressure on housing costs. This ongoing supply challenge, coupled with strong population growth, suggests that the market may continue to experience tight conditions and price increases in the foreseeable future.

This brings us to housing affordability challenges, particularly for first home buyers. In the past twenty years, the CoreLogic Home Value Index has increased by about 150%, a stark contrast to the ABS Wage Price Index, which has seen an 82% rise, according to CoreLogic. This significant gap between the growth in home prices and wages illustrates the escalating difficulty that new entrants face when trying to access the housing market. Such trends underscore the need for careful consideration of market entry strategies and timing for potential homeowners.

As 2024 progresses, the landscape of the housing market is shaped by both promising opportunities and notable challenges. Investors and business owners can thrive by closely monitoring the distinct characteristics of their local markets, staying up-to-date with broader economic trends, and being responsive to changes in consumer confidence. Despite the challenges posed by high interest rates and the cost of living, the housing market's robustness offers substantial opportunities for strategic investments. For those ready to navigate its complexities, the housing market remains a fertile ground for growth and investment, promising valuable returns for the well-informed and proactive participant.

Inflation and Interest Rates

At its last meeting (19 March 2024), the Reserve Bank of Australia (RBA) maintained the cash rate target at 4.35% and kept the interest rate on Exchange Settlement balances at 4.25%. This decision was influenced by a continued, albeit moderating, high level of inflation impacting the cost of living across the country. Despite a steadying Consumer Price Index (CPI) at 3.4% year-on-year to January, service costs remain elevated, reflecting ongoing demand and cost pressures within the economy.

The labor market is showing signs of easing, yet remains tighter than desired for achieving full employment targets. The slight uptick in wage growth during the December quarter is expected to moderate, aligning with the RBA's forecast and reflecting the delayed impact of previous rate hikes on economic activities. According to NAB’s recent findings, The outlook for real wage growth is bleak, with expectations of slow improvements due to the low productivity growth. This scenario underscores the necessity for wage adjustments to closely track productivity gains to maintain economic stability and prevent inflationary pressures.

The U.S. Federal Reserve's stance mirrors that of the RBA, with interest rates held steady at 5.25-5.5%. The U.S. economy continues to demonstrate resilience, distinguishing itself from other major economies facing recessionary pressures. This strength is backed by favorable inflation figures that, while slightly above the Fed's 2% target, have shown significant improvement from the previous year's highs. The robustness of the U.S. market provides a stark contrast to the ongoing economic challenges in the UK, Europe, and Japan, reinforcing its critical role in the global economic framework.

In Europe, the European Central Bank's decision to maintain interest rates suggests a cautious optimism that the peak of the interest rate cycle may have been reached. This is a critical phase as Europe grapples with a complex economic recovery pathway.

Meanwhile, Japan's economy shows signs of strain despite narrowly avoiding a recession. The Bank of Japan's recent policy adjustments, including the first interest rate hike since 2007 and the cessation of yield curve control, signal a strategic shift in response to a break from deflation and modest wage growth. Alongside the interest rate hike, the Bank of Japan has ended its yield curve control program and its purchases of exchange-traded funds and real estate investment trusts, indicating a reduced need for market support.

China's ambitious GDP growth targets amidst a faltering property sector and low housing confidence pose potential challenges for Australia, given the deep trade links between the two nations. A slowdown in China could impact the demand for Australian exports like iron ore and coal, thus affecting Australia's trade balance and broader economic health.

The global economic environment remains fraught with uncertainty, impacting consumer behavior and business planning across Australia. Household spending in Australia is tepid, influenced by inflationary pressures and previous interest rate rises. However, the RBA remains committed to returning inflation to its 2-3% target range by 2025, focusing on long-term economic stabilisation and ensuring that Australians can manage their financial futures with greater certainty. The international economic landscape will continue to play a significant role in shaping domestic economic strategies and outcomes.