Annual Financial Planning Checklist 2024

A personal financial plan involves assessing your current financial status comprehensively. This includes evaluating all your assets, such as your income, savings, transaction accounts, and retirement fund. Additionally, you also need to consider your liabilities, loans, credit card balances, and other personal debts. It's essential to also factor in recurring expenses like mortgage or rent payments, utility bills, and other monthly financial obligations.

This financial snapshot should also integrate your goals and the necessary steps to achieve them. These objectives may span various areas such as retirement planning, tax management, and investment strategies. By incorporating these goals into your plan, you can ensure that your financial decisions align with your long-term aspirations.

This checklist comprises the crucial steps in reviewing your annual financial plan. Mark off each step as you complete it, regardless of whether you opt not to refinance your mortgage or have already cleared your credit card balances. This approach aids in obtaining a comprehensive overview of your finances.

Step 1: Conduct a Personal Financial Inventory

An annual personal inventory provides a snapshot of your financial standing, facilitating year-to-year progress comparison. Whether you have last year's inventory or are starting fresh, follow these steps:

- List your assets and their respective amounts, including, savings, retirement account values, and real estate.

- List your debts, encompassing your mortgage, car loan, student loans, and credit card balances.

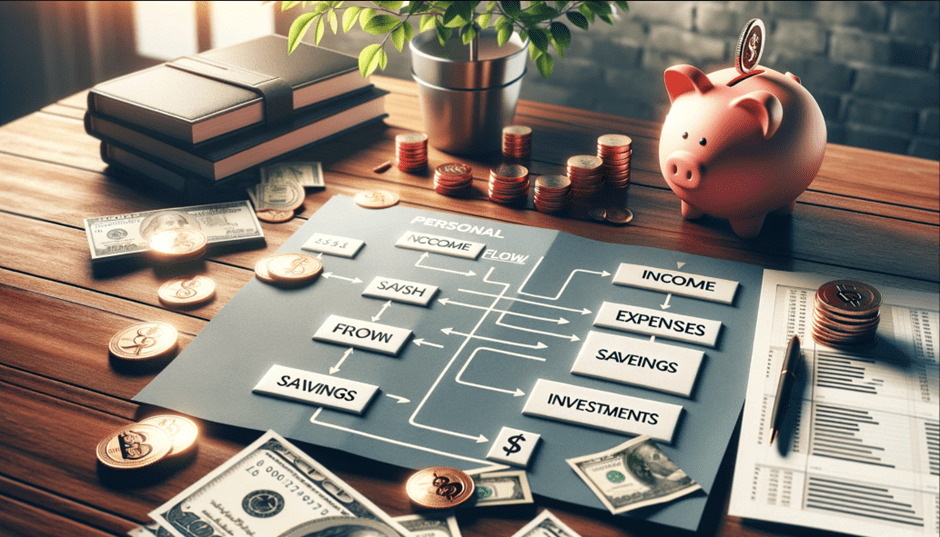

Step 2: Understand Your Cash Flow

Understanding the inflow and outflow of your finances is pivotal. The initial and arguably most crucial step towards financial wellness is crafting a budget to effectively manage your income and expenditures. Utilizing budgeting applications can aid in monitoring your financial transactions, preventing overspending.

- List all income sources including work, self employment and investment income

- List all expenses including living expenses, mortgage repayments, business expenses and costs associated investments (e.g. investment property expenses)

Do you expect significant changes to your income and expenses in the upcoming year?

Step 3: Establish Financial Objectives

Before embarking on the journey towards your dreams, it's essential to identify and outline them. Deliberating over your financial objectives and documenting them brings them closer to fruition. Your financial goals typically fall into three distinct categories: short-term, medium-term, and long-term.

Short-term Goals:

These are immediate goals between 1-5 years. Examples include:

- Setting up a budget to manage cash flow

- Establish or bolster an emergency fund of $50,000 to enhance financial security

- Prioritize clearing credit card debts.

- Saving for a new car approx. $80,000

- Family vacation $10,000

- New hobby $5,000

Mid-term Goals:

These objectives aim to be achieved within the next 10 years. Examples include:

- Saving for a down payment on your first home $150,000

- Acquiring life and disability insurance to safeguard against unforeseen circumstances

- Pursue a graduate degree to advance your career

- Property renovations

- Funding children's education

Long-term Goals:

Looking further ahead, envision your financial position in the subsequent 20 or 30 years. Examples include:

- Downsizing your home after your children have left the nest

- Early retirement around age 60 instead of 67

- Acquiring a holiday home

- Estate planning

Step 4: Develop a Family Financial Strategy

Life is filled with both anticipated milestones and unforeseen challenges, all of which necessitate careful financial planning. Whether it's purchasing your first home, starting a family, transitioning careers, or retiring, strategic financial management is essential. Additionally, unexpected events like job loss or the death of a spouse can arise suddenly, underscoring the importance of financial preparedness for you and your loved ones. Here are some essential items to address:

College Savings for Children

How do you intend to finance your children's college education? Have you devised a savings plan or explored other options?

Assessing Insurance Needs for Yourself and Your Spouse

Consider acquiring long-term care insurance or life insurance policies to secure financial stability for yourself and your spouse.

Debt management

Consider paying off high interest debt and non deductible debt, and consolidate debt to make finances more manageable.

Retirement Planning

Are you on target with your retirement planning? Have you and your spouse established retirement goals and considered avenues like annuities to ensure a guaranteed stream of income during retirement?

Estate Planning

Ensure your instructions are followed by getting your wills drafted. This allows for the smooth transition of assets while minimizing the potential for family disputes and ensuring their legacy endures.

Step 5: Set up an emergency fund

The importance of having an emergency fund cannot be overstated. Are you prepared for unforeseen life events such as a prolonged illness or job loss? Establishing an emergency fund is a prudent step towards financial preparedness, providing a safety net for unexpected expenses. Financial experts typically recommend saving three to six months' worth of fixed living expenses—such as rent or mortgage payments, food costs, and transportation—in an emergency fund. It's crucial to keep this fund liquid, preferably in a savings or money market account, to ensure immediate access in times of need. By prioritizing the creation of an emergency fund, you can gain peace of mind, knowing that you have a financial cushion to weather life's uncertainties.

Step 6: Plan NOW for Retirement

Whether you're in your early career stages or nearing retirement age, initiating retirement savings is imperative. The earlier you commence this financial journey, the greater the benefits of compound interest in maximising your investments over time. Things you can do now include:

- Increase super contributions.

- Understand your super – investment options, asset allocation, fees – are you getting the most out of your investment?

Step 7: Build and alternate income stream

In addition to super, exploring additional income sources can enhance financial security during retirement. Consider alternative avenues to supplement your income:

Rental Property Investment

Generate regular income by investing in rental properties and becoming a landlord. This venture offers steady cash flow and the potential for long-term appreciation.

Part-Time Employment

Explore part-time job opportunities, especially with the rise of remote work options. Finding a flexible job can bolster your primary income and provide additional financial stability.

Investment Portfolio

An investment portfolio outside of superannuation can serve as a valuable resource to fulfill shorter-term financial requirements, such as funding education expenses or purchasing a new vehicle.

Unlike property investments, an investment portfolio offers greater liquidity, enabling easier access to funds when needed.

By maintaining a well-balanced investment portfolio, you can effectively address various financial objectives while optimizing wealth accumulation.

Step 8: Protect yourself and your family

As you conduct your financial review, it's essential to reassess your insurance coverages. Yearly evaluations of home insurance policies are crucial to ensure adequate coverage in the event of damage or loss.

Additionally, it's vital to review your coverage for accidents or disabilities, as these unforeseen events can significantly impact your financial future. By proactively managing your insurance policies, you can protect yourself from financial hardship and ensure peace of mind for the future.

Step 9: Review Annually

As you embark on a new year filled with celebrations and gatherings, it's essential to pause and review your financial standing, particularly your investment objectives. Whether you choose to undertake this review in January or at another point during the year, conducting an annual assessment of critical financial components is invaluable. Take the time to reassess your insurance coverage, and scrutinize your investments, with a particular focus on your retirement accounts. By consistently monitoring these key financial aspects, you can ensure alignment with your goals and aspirations while fostering financial stability for the future.

Financial Planning Checklist

Feel free to download it now to serve as a foundational resource when meeting with your adviser. It can assist you in identifying key components necessary to optimise your financial strategy.