Newsletter – August 2024

The Share Market

August 2024 was a mixed month for share markets in Australia and the US. The ASX 200 posted a modest gain, showing cautious optimism among investors, while the US S&P 500 trended upward ahead on the back of positive economic news. Let’s look at what happened in these markets, the factors that influenced their performance, and what it means for investors.

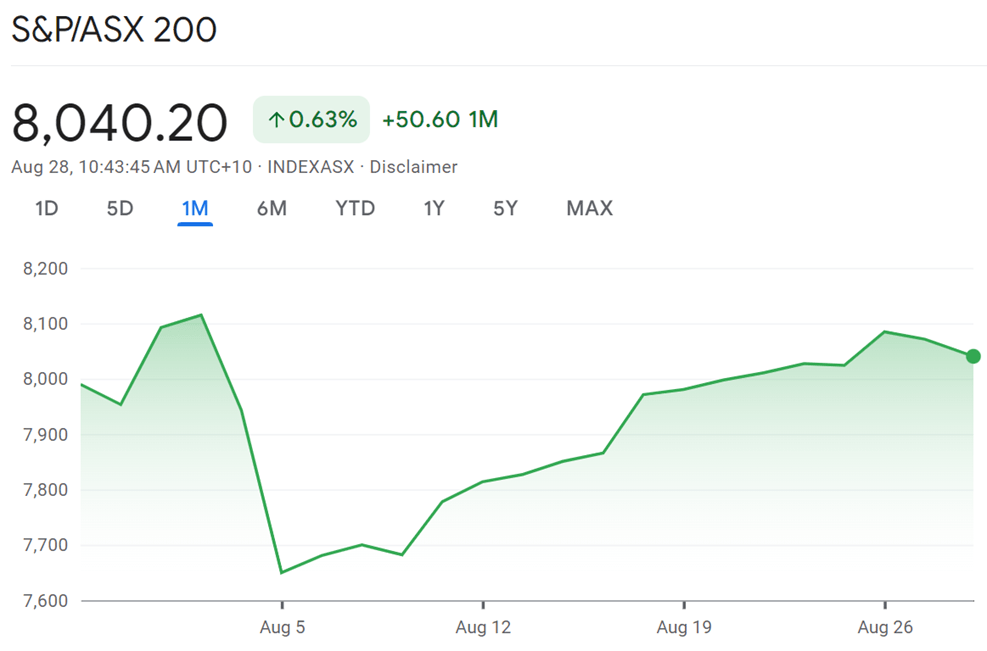

The ASX 200 closed at just over 8,040 towards the end of August, up by 0.63% for the month. The index saw a lot of ups and downs, starting strong with a peak around 8,150 before dropping sharply to just under 7,700. A steady recovery followed in the second half of the month.

One of the most significant influences on the ASX 200 was the release of the latest inflation data. On August 28, figures for July 2024 showed annual inflation at 3.5%, a decrease from June's 3.8% but slightly above the anticipated 3.4%. This news caused an immediate ripple effect, with the ASX 200 dropping 0.2% within minutes of the announcement. The persistence of inflation, albeit at a reduced rate, raised questions about the future direction of monetary policy.

The Reserve Bank of Australia's (RBA) policy stance was another key factor. The RBA held the cash rate at 4.35% in August, but concerns about potential future rate hikes lingered. Higher interest rates typically raise borrowing costs, which can slow down the economy and impact company profits. This uncertainty kept investors on edge, leading to a more cautious recovery compared to other global markets.

August also saw the release of numerous company earnings reports, which had varying impacts on individual stocks and broader sectors. A notable example was WiseTech Global, which experienced a remarkable 18.3% surge from its 2024 financial year result in August following positive broker upgrades in response to its earnings report. These individual performances contributed to the overall market dynamics, with some sectors outperforming others.

Sector performance was mixed throughout the month. Energy and mining stocks showed strength in late August, buoyed by global commodity trends. In contrast, the financial sector faced challenges, possibly due to concerns about the economic outlook and interest rate trajectories. The IT sector presented a mixed picture, with companies like WiseTech Global posting significant gains while others, such as Megaport, experienced declines.

Despite these various influences, the overall trend for the ASX 200 in August was positive. The index approached its all-time high of $8,148, having rallied over 5.3% from its early August low of $7,628. This upward momentum culminated in a four-week high of $8,107 on August 27, before a slight easing occurred.

Global factors also played a role in shaping the ASX 200's performance. Notably, anticipation surrounding Nvidia's earnings report on August 28 influenced market sentiment, highlighting the interconnectedness of global markets and the impact of major international companies on Australian stocks.

Despite these challenges, there were some bright spots. Consumer spending remained resilient, with retail and discretionary sectors showing stronger-than-expected results. This supported the overall market and helped offset losses in resource-heavy areas.

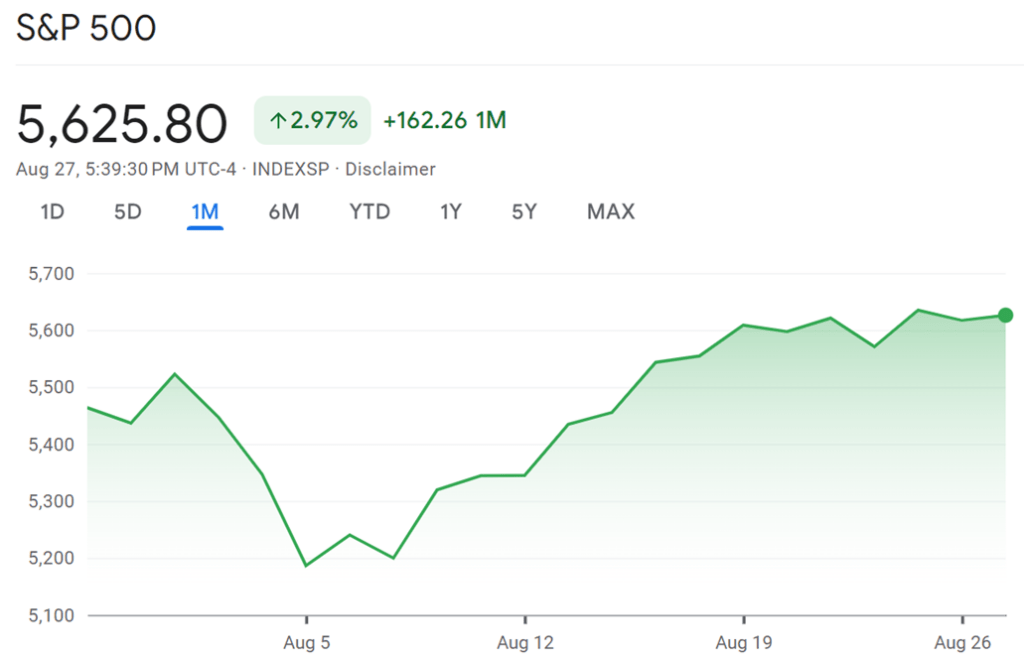

The US S&P 500 performed much better, gaining 2.97% to close at $5,625.80 on August 27, 2024. The main driver was better-than-expected economic data, particularly around inflation. The latest Consumer Price Index (CPI) data showed inflation at 2.9% for the 12 months ending July 2024, which, while still above the Federal Reserve’s target, was lower than many had expected. This helped ease worries about aggressive interest rate hikes, boosting investor confidence.

One of the primary drivers of market sentiment was the anticipation of potential interest rate cuts by the Federal Reserve. Federal Reserve Chair Jerome Powell's statement that "the time has come" for a relaxation of monetary policy signaled a likely rate cut in September, fueling investor confidence. This shift in monetary policy expectations played a significant role in shaping market trends throughout the month.

Economic data releases continued to be crucial in guiding investor behavior. Particular attention was focused on the upcoming July Personal Consumption Expenditures (PCE) price index, the Fed's preferred measure of inflation, scheduled for release at the end of the month. The downward trend in this index over recent months had been a key factor in bolstering market sentiment and influencing Fed policy expectations.

Corporate earnings, especially from the technology sector, were another major influence on the S&P 500's performance. The market eagerly anticipated Nvidia's earnings report, scheduled for late August. With Nvidia's stock having surged an impressive 181% year-to-date, its performance was seen as a bellwether for the artificial intelligence sector and the tech industry at large. On August 28, Nvidia posted record quarterly Data Center revenue of $26.3 billion, up 154% from a year ago. However, the forecast for the third quarter was less optimistic, leading to a decline in Nvidia’s stock and affecting other tech stocks.

The technology sector's performance remained a significant factor in the index's movements. While some mega-cap stocks like Apple, Microsoft, Amazon, and Meta Platforms showed signs of weakness in premarket trading, others such as Alphabet managed to make gains. This mixed performance within the tech sector added an element of complexity to the overall market narrative.

Global market events also played a role in shaping the S&P 500's trajectory. Earlier in the month, a sharp decline in Japan's Nikkei 225 index had ripple effects on U.S. stocks, highlighting once again the interconnected nature of global financial markets.

Notably, fears of a potential recession that had loomed over the market earlier in the year had largely subsided by August. This improved economic outlook contributed significantly to the market's recovery from its early August decline and supported the overall positive trend.

The artificial intelligence sector continued to be a focal point for investors, driving enthusiasm and investment in related companies. This ongoing AI boom, exemplified by the anticipation surrounding Nvidia's earnings, underscored the technology sector's pivotal role in market dynamics.

When comparing the ASX 200 and S&P 500, it’s clear that the US market outperformed Australia’s. The S&P 500’s gain of nearly 3% stands out against the ASX 200’s modest 0.63% rise, reflecting differing investor sentiment. One of the main reasons for this gap is the contrasting economic conditions. The US is beginning to see inflation ease, whereas Australia still faces uncertainty about future rate hikes from the RBA.

The structure of the two indices also plays a role. The ASX 200 has a heavy focus on resources and financial companies, which are highly sensitive to global commodity prices and economic conditions. In contrast, the S&P 500 is more weighted towards tech and consumer stocks, which have been doing well recently.

Geopolitical factors, such as trade tensions and supply chain issues, continue to affect Australian companies, especially those in the export business. These challenges add another layer of pressure on the ASX 200.

Staying informed and maintaining a diversified portfolio will be key strategies for managing the uncertainties that lie ahead in global markets.

The Residential Property Market

The residential property market in Australia has shown notable changes as of August 2024. While home values have generally increased, there are significant differences between various cities and regions. Let’s look at the detailed overview of the latest trends and developments, based on CoreLogic Monthly Housing Chart Pack published in early August 2024.

National Overview

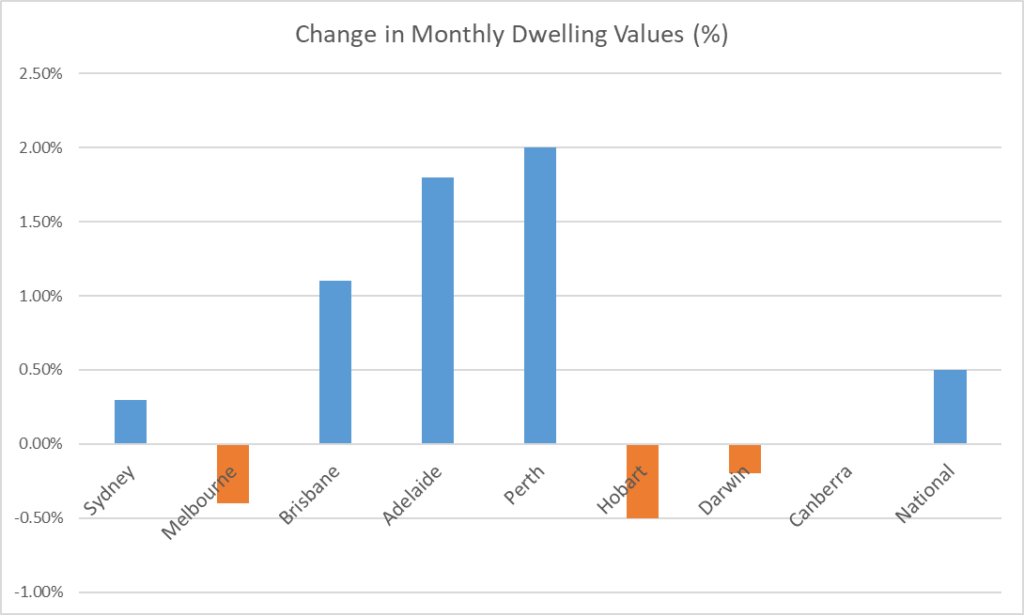

The national Home Value Index (HVI) rose by 0.5%, marking the 18th month of continuous growth. This increase follows a significant drop of 7.5% from May 2022 to January 2023, resulting in an overall gain of 13.5% since then. Home values are now at their highest since November 2023. However, this overall positive trend hides some declines in specific areas.

Growing Markets

Several cities showed positive growth:

- Perth: Strongest performer with a 2% monthly increase

- Adelaide: Close second with 1.8% growth

- Brisbane: Solid growth at 1.1%

- Sydney: Modest increase of 0.3%

Declining Markets

Some cities experienced a drop in home values:

- Melbourne: Declined by 0.4%

- Hobart: Fell by 0.5%

- Darwin: Slight decrease of 0.2%

- Canberra remained stable with no change (0.0%).

Regional Markets

Regional housing values are not keeping pace with capital cities, showing a quarterly rise of only 1.3%. However, some regions are performing well:

- Regional Western Australia: Up by 4.7%

- Regional South Australia: Up by 3.2%

- Regional Queensland: Up by 2.8%

- Regional Victoria, however, saw a decline of 1.4%.

Supply and Demand

The number of homes for sale varies widely across the country. Cities like Brisbane, Adelaide, and Perth have fewer homes available, which supports price growth. In contrast, Melbourne and Hobart have higher supply levels, leading to price drops.

Affordability Issues

Rising home prices are pushing buyers towards more affordable options. The lower end of the market is seeing more growth than the higher end, with lower-priced homes increasing by 3.3% compared to just 0.8% for higher-priced homes.

Rental Market Trends

Rental growth is slowing, with only a 0.1% increase in July, the smallest rise since August 2020. Some cities, including Sydney and Brisbane, even saw slight declines in rents. This slowdown is particularly noticeable in the unit rental market, where annual growth rates have dropped significantly.

Investment Activity

Investor interest is on the rise, with loans for investment properties up by 24.8% compared to last year. However, many investors are facing challenges due to the gap between mortgage rates and rental yields, which has widened considerably.

Future Outlook

The housing market outlook is mixed. While limited new housing supply is likely to support prices, affordability is becoming a growing concern. The ratio of home values to income is nearing record highs, making it harder for many buyers to enter the market.

As we move forward, the residential property market will continue to show varied trends across different regions, with some areas thriving while others face challenges.

Inflation and Interest Rates

In August 2024, Australians are still feeling the pinch of higher prices, but there's a glimmer of hope on the horizon. Let's take a closer look at what's happening with inflation and interest rates, and what it means for everyday people.

Inflation: The Slow Cool-Down

Inflation has been a hot topic in Australia for the past few years. The good news is that it's cooling down, but not as quickly as many would like. In July 2024, the yearly inflation rate dropped to 3.5%, down from 3.8% in June. This is the lowest it's been since March 2024, which is a step in the right direction.

One of the main reasons for this drop was a 5% decrease in electricity costs, thanks to government rebates. That's a welcome relief for households struggling with high energy bills. However, the Reserve Bank of Australia (RBA) still thinks inflation is too high. They want to see it between 2% and 3%, so there's still some way to go.

Interest Rates: Holding Steady for Now

The RBA decided to keep it at 4.35% in August. This rate, known as the cash rate, influences the interest rates that banks charge on loans and offer on savings accounts. The RBA is being careful not to change rates too quickly. They're worried that if they lower rates too soon, inflation might start rising again. On the other hand, if they keep rates high for too long, it could slow down the economy too much.

What This Means for You

If you have a mortgage, you might be wondering when you'll see some relief from high interest rates. Unfortunately, it looks like you might have to wait a bit longer. Three of Australia's biggest banks think the RBA won't start lowering rates until 2025. Only one major bank, Commonwealth Bank, thinks a rate cut might happen in late 2024.

For savers, the news is a bit better. High interest rates mean you're probably earning more on your savings accounts than you were a couple of years ago. However, with inflation still above 3%, the value of your savings is still being eaten away somewhat.

The Bigger Picture

The RBA expects the Australian economy to grow faster in 2025. They also think the job market will stay strong, even though it might ease up a bit. This is good news for workers, as it means jobs should still be relatively easy to find.

As for inflation, the RBA now thinks it will take longer to get back to their target range. They're predicting it won't be until 2026 that inflation will be comfortably between 2% and 3%.

What's Next?

For now, it seems Australians will need to be patient. The RBA is working hard to bring inflation down without causing too much economic pain. They're watching the economy closely and will adjust interest rates if needed. In the meantime, it's a good idea to keep an eye on your budget. If you have debts, especially a mortgage, it might be worth checking if you're getting the best deal. For savers, shopping around for the best interest rates on savings accounts could help you make the most of the current high-rate environment.