Newsletter – July 2024

The Share Market

In July 2024, both the ASX 200 and the S&P 500 showed positive performance, reflecting overall optimistic market sentiment.

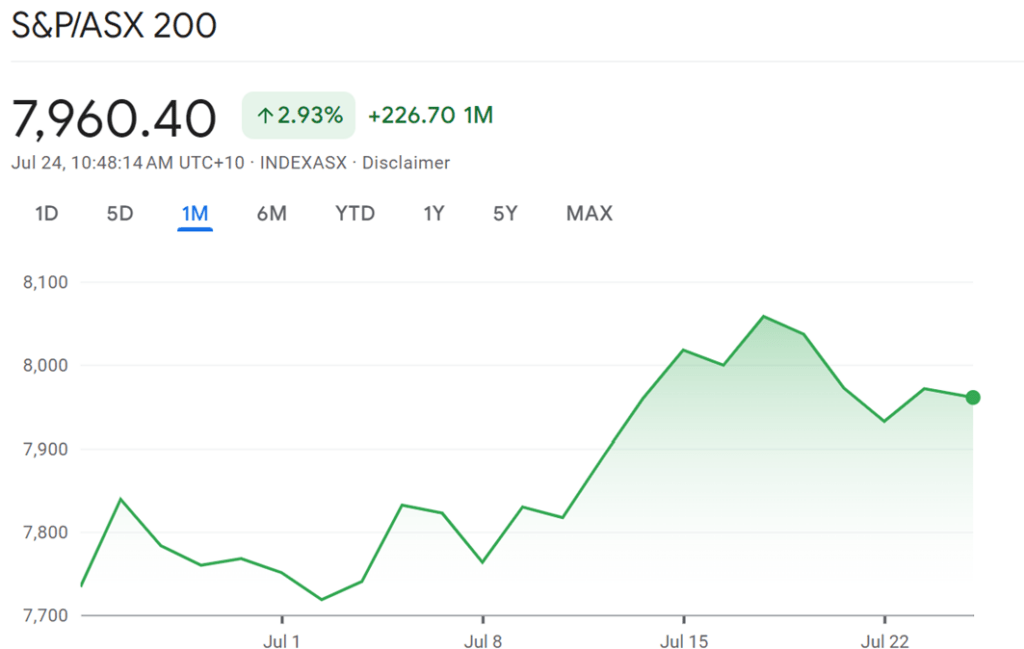

The ASX 200 closed at 7,960.40, marking a 2.93% increase from the previous month. This growth represents a gain of 226.70 points. Throughout the month, the ASX 200 started around 7,700 points and experienced various ups and downs. However, it maintained a general upward trend, hitting a new record high near 8,050 points in mid-July before settling at its closing value.

The gains were broad-based across sectors, with particularly strong performances in IT, healthcare, and banking stocks. Despite concerns about stubborn inflation and the potential for additional interest rate hikes by the Reserve Bank of Australia, the market demonstrated overall strength, supported by positive global sentiment and sector-specific developments.

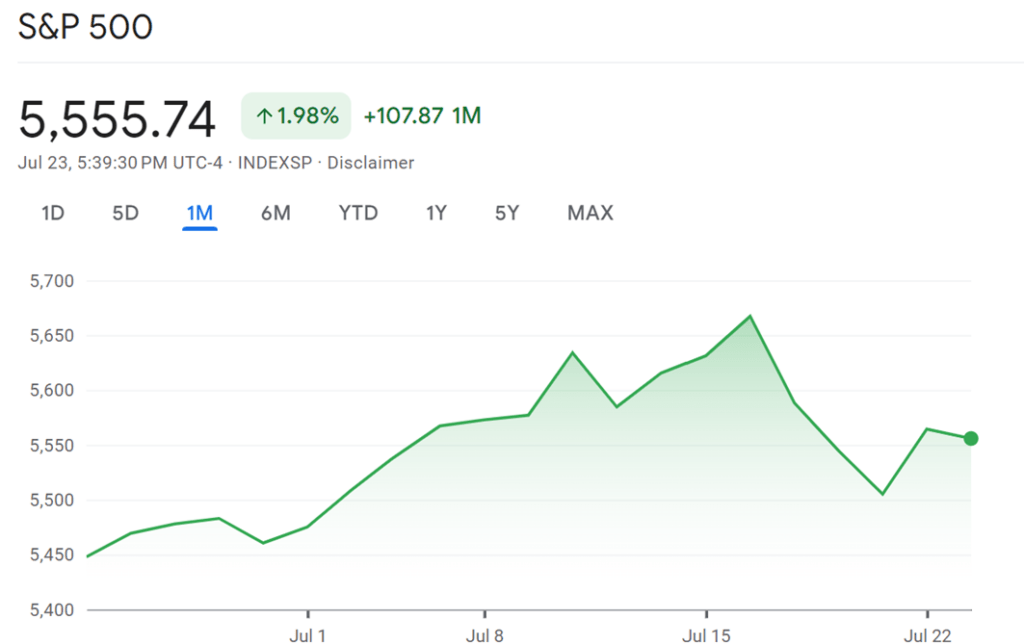

On the other side of the globe, the S&P 500 also had a positive month, closing at 5,555.74, which is a 1.98% increase, or 107.87 points up from June. The index began July at approximately 5,450 points and followed a consistent upward trajectory, peaking near 5,650 points by mid-July. Despite a three-day consecutive dip in the third week, it recovered to finish relatively strong at 5,555 points.

The S&P 500 was primarily driven by a rebound in tech shares, with investors returning to high-flying tech stocks after a brief rotation into smaller companies. The market showed resilience in the face of political changes, including President Biden's withdrawal from the election race, which had only a muted impact. The tech sector, particularly semiconductor companies played a significant role in boosting the index. Despite some short-term volatility, the S&P 500 maintained its long-term upward trajectory, reflecting ongoing investor optimism and market stability.

When comparing the two indices, the ASX 200 outperformed the S&P 500, with a nearly 1% higher gain. The ASX 200 also displayed more significant fluctuations compared to the more stable S&P 500. However, both markets ended on a positive note, suggesting a robust global economic environment. The overall upward trends imply that investors are confident, with the Australian market showing particularly strong sentiment.

In summary, July 2024 was a strong month for both the ASX 200 and the S&P 500. The Australian market, in particular, showed robust performance, indicating strong investor confidence. This positive market activity reflects a broader optimism about economic conditions and future growth prospects. Investors can take comfort in the steady rise of both indices, reflecting stable and improving economic environments in both Australia and the US.

2024 Financial Year in Review

As the new financial year begins, reviewing last year’s market performance provides valuable insights into trends, helps identify potential opportunities, and prepares investors for informed decision-making in the year ahead.

Despite high inflation and interest rates, both the ASX 200 and the S&P 500 have shown resilience and delivered positive returns in the 2024 financial year.

The ASX 200 grew by 9%. This steady growth was helped by strong demand for Australian commodities like iron ore and energy. The Reserve Bank of Australia’s careful approach to raising interest rates also kept investor confidence high. Sectors such as mining and energy did well, balancing out weaker areas like financials and consumer goods.

The S&P 500 saw a larger increase of 21.98%, mainly driven by the tech sector. Big tech companies reported strong earnings and continued to innovate, which attracted investors. The Federal Reserve’s handling of interest rates and hints of future rate cuts also boosted the market. Earnings growth across various sectors, especially in technology and consumer goods, contributed to the strong performance.

High inflation usually reduces purchasing power and increases business costs. However, companies that can pass these costs to consumers or those in less affected sectors, like technology, tend to do better. Higher interest rates make borrowing more expensive, which can slow economic growth. Despite this, markets have remained strong due to solid corporate earnings, particularly in tech, and positive investor sentiment driven by expectations of future rate cuts and economic stability.

The Residential Property Market

The Australian residential property market has shown continued resilience and growth in July 2024, despite facing several economic challenges. Let’s look at the detailed overview of the latest trends and developments, based on CoreLogic Monthly Housing Chart Pack for July 2024.

Capital City Performance

- Sydney's housing market grew by 0.5% in June 2024, with a quarterly rise of 1.1% and an annual growth of 6.3%. The total return stands at 9.6%, with the median dwelling value reaching $1,170,152.

- Melbourne saw a slight decline of 0.2% in June, with a quarterly drop of 0.6%. However, annual growth remains positive at 1.3%. The total return is 4.9%, and the median value is $783,205.

- Brisbane's market showed strength with a 1.2% increase in June. Quarterly growth is 3.7%, and annual growth is 15.8%. The total return is an impressive 20.5%, with the median value at $859,240.

- Adelaide experienced robust growth of 1.7% in June. Quarterly growth is 4.7%, and annual growth is 15.4%. The total return is 20.0%, with the median value now $767,974.

- Perth led the capital cities with a 2.0% increase in June. Quarterly growth is 6.4%, and annual growth is 23.6%. The total return is 29.5%, with the median value at $757,399.

- Hobart showed modest growth of 0.1% in June, but quarterly and annual changes are slightly negative. The total return is 4.0%, with the median value at $645,850.

- Darwin's values remained stable in June, with no monthly change. Quarterly growth is 1.0%, and annual growth is 2.4%. The total return is 9.0%, with a median value of $504,687.

- Canberra saw a 0.3% increase in June. Quarterly growth is 0.8%, and annual growth is 2.2%. The total return is 6.4%, with the median value at $870,071.

National Overview

Australian dwelling values increased by 0.7% in June, bringing the total growth for the financial year 2023-24 to 8.0%. This growth is equivalent to a $59,000 increase in the median dwelling value. Despite high interest rates, cost of living pressures, and tight credit policies, the housing market has remained robust due to tight supply levels, which continue to exert upward pressure on property values.

Key Factors Influencing the Market

- Population Growth: Australia’s population grew by 624,100 people over the year to December 2023, the largest increase since 2008. This strong population growth continues to underpin housing demand.

- Supply Constraints: Despite efforts to increase housing stock, supply constraints persist. Total listings are 17.3% lower than the historic five-year average, contributing to ongoing value increases nationally.

- Interest Rates: Economists and financial institutions suggest that interest rates are likely to either remain steady or potentially increase in the coming months (see next section on Inflation and Interest Rates).

- Rental Market Dynamics: The rental market has shown signs of easing, particularly in major capitals. The annual growth rate in capital city unit rents has slowed significantly, with Sydney, Melbourne, and Brisbane experiencing the most notable declines. This slowdown likely reflects an easing in demand amid early signs of slowing net overseas migration.

Challenges and Concerns

- Affordability Issues: The continued rise in property values is exacerbating affordability concerns, particularly for first-time buyers in major cities. Mortgage affordability is now at its worst since 1990, which may slow down the housing market’s growth rate.

- Market Fragmentation: The property market is becoming more fragmented, with varying performance across different regions and property types. This fragmentation may lead to increased inequality in housing opportunities.

Outlook for the Remainder of 2024

The outlook for the Australian housing market remains generally positive, with expectations of continued growth, albeit at a potentially slower pace. Factors such as strong population growth and supply constraints are likely to support the market. However, affordability concerns, potential rate hikes and economic uncertainties may moderate the growth trajectory in some areas.

In conclusion, the Australian residential property market has demonstrated remarkable resilience and adaptability in the face of economic challenges. The market continues to grow, driven by strong population growth and persistent supply constraints, although affordability issues remain a significant concern.

Inflation and Interest Rates

In July 2024, the Reserve Bank of Australia (RBA) did not hold a meeting. The cash rate remains at 4.35%, a level it has maintained since November 2023. The next cash rate announcement is scheduled for early August 2024.

As the RBA prepares for its next cash rate announcement, market predictions and economic forecasts provide a mixed outlook on potential rate movements:

- Steady Cash Rate Expected: Many economists and financial institutions predict that the RBA will maintain the cash rate at its current level of 4.35%. This expectation is based on the belief that the current rate is sufficiently restrictive to manage inflation without further hikes. The big four banks, including ANZ, CommBank, NAB, and Westpac, largely agree that the cash rate has peaked and will likely remain unchanged until late 2024 or early 2025.

- Potential for Rate Hikes: Despite the consensus on a steady rate, some analysts, such as Warren Hogan from Judo Bank, anticipate further rate hikes. Hogan predicts that the RBA might implement up to three additional 0.25 percentage point increases by the end of the year, potentially raising the cash rate to 5.10%. This view is driven by concerns that the current strategy of holding rates steady may not be sufficient to curb persistent inflation.

Inflation

As of July 2024, Australia's inflation rate remains elevated at 3.8%, slightly higher than the 3.6% reported in the previous month. This persistent inflation is above the RBA's target range of 2-3%, indicating ongoing price pressures in the economy. The central bank has acknowledged that the process of returning inflation to the target range is unlikely to be smooth, with recent data showing a slower-than-expected decline in inflation.

Economic Context

The Australian economy has shown signs of slowing growth, with the second quarter of 2024 recording a meager 0.1% growth rate, similar to the first quarter. This sluggish growth is indicative of the broader economic challenges, including high interest rates and subdued consumer spending. The unemployment rate has risen slightly to 4.2%, reflecting a gradual easing in the labor market.

Future Outlook

The RBA has indicated that it remains open to further rate hikes if inflationary pressures persist. The next significant data point will be the consumer price inflation for the June quarter, which will provide a more comprehensive view of the inflationary trends and is expected to be available by the end of July.

Conclusion

The market prediction for the RBA's August 2024 cash rate decision leans towards maintaining the current rate of 4.35%. However, there remains a possibility of further rate hikes if inflation data continues to show persistent price pressures. We will closely monitor the announcement and share our insights next month.