Newsletter – June 2024

The Share Market

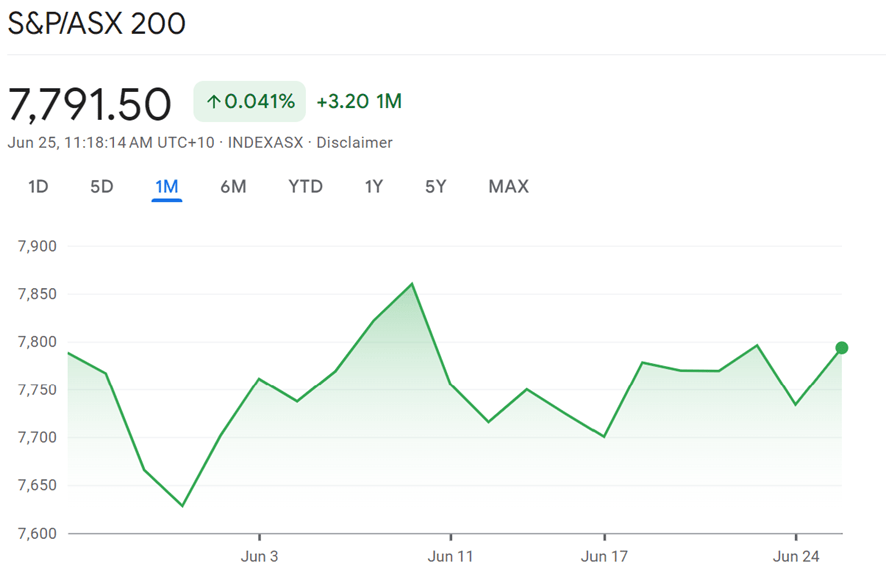

In June 2024, the ASX200 index showed resilience despite market fluctuations. At the beginning of the month, it hovered just below 7,750. Around June 11th, the index briefly surpassed 7,800. However, it experienced a slight dip afterward. By June 25th, the index had recovered, closing at approximately 7,791.50. The modest increase of 3.20 points (0.041%) from the previous value suggests stability and potential growth for shareholders.

Several key events and factors impacted the performance of the ASX 200.

The ASX 200 experienced a lack of positive influence from US equity markets, particularly on days when the US markets were closed, such as for the Juneteenth holiday. This led to a slight decline in the ASX 200 on June 20, 2024, where it traded 12 points lower at 7758.

The Reserve Bank of Australia's decision to keep interest rates on hold at 4.35% for the fifth consecutive meeting provided some stability. However, the RBA noted that inflation was easing more slowly than expected, which kept the market cautious. This decision helped the ASX 200 rebound strongly on June 18, 2024, with a 0.90% increase to 7769.

Other sector-specific movements also influenced the market. The debut of Guzman y Gomez on the ASX was a significant event, with its share price opening well above the IPO price, indicating strong investor interest. On the other hand, the banking sector saw mixed performances, with some banks hitting record highs while others experienced modest gains.

The ASX200 displayed a more stable and modest growth pattern. While it did experience some fluctuations, the overall trend was one of resilience and steady progress. The Australian index's performance was supported by gains across various sectors.

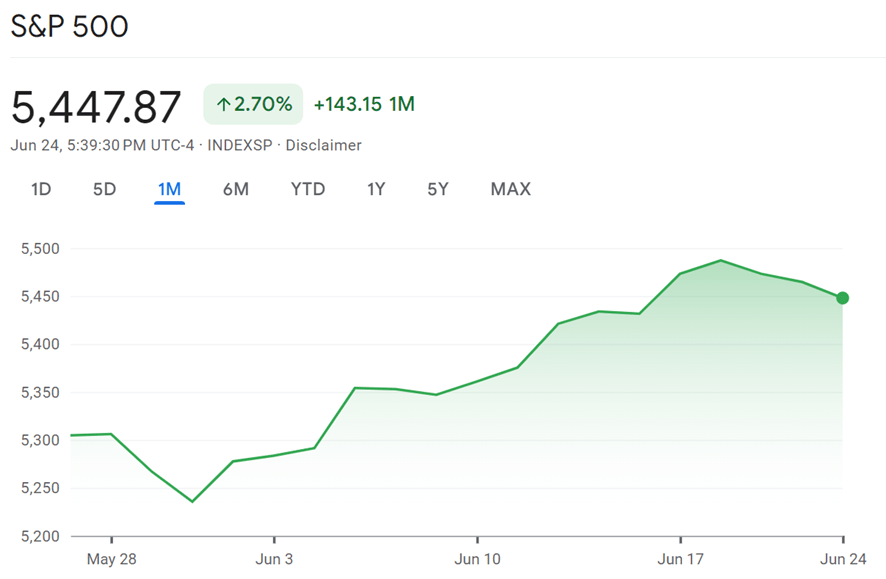

On the other hand, the S&P 500, a key index representing the U.S. stock market, exhibited mixed performance in June 2024. As the market approached the end of the first half of the year, the S&P 500 reached new all-time highs, with the index hitting an intraday peak of 5,505.53. This milestone capped off a strong performance, with the S&P 500 gaining nearly 15% year-to-date and achieving 31 record closes in 2024.

The S&P 500, a key index representing the U.S. stock market, exhibited mixed performance in June 2024. As the market approached the end of the first half of the year, the S&P 500 reached new all-time highs, with the index hitting an intraday peak of 5,505.53. This milestone capped off a strong performance, with the S&P 500 gaining nearly 15% year-to-date and achieving 31 record closes in 2024.

Despite the overall positive trend, the market showed signs of fatigue towards the end of June. On June 24, 2024, the S&P 500 experienced a slight decline, closing 0.3% lower for the day. This downturn was primarily driven by a selloff in the technology sector, particularly among chip companies.

The market's performance was influenced by several factors. The excitement surrounding artificial intelligence continued to buoy investor sentiment, contributing to the significant gains seen throughout the year. However, concerns about market exhaustion began to emerge, especially in light of the recent decline in Nvidia's stock, a key player in the AI-driven rally.

Investors remained focused on upcoming economic data, particularly the May personal consumption expenditure data scheduled for release on June 28, 2024. This key inflation indicator, favored by the Federal Reserve, was expected to provide insights into the economic landscape and potential future interest rate decisions.

As the market moved into the latter part of June, there was a noticeable rotation of investor interest. While technology stocks, especially chip makers, experienced declines, other sectors such as energy and financials saw gains. This shift highlighted the evolving dynamics of the market as it navigated through economic uncertainties and changing investor preferences.

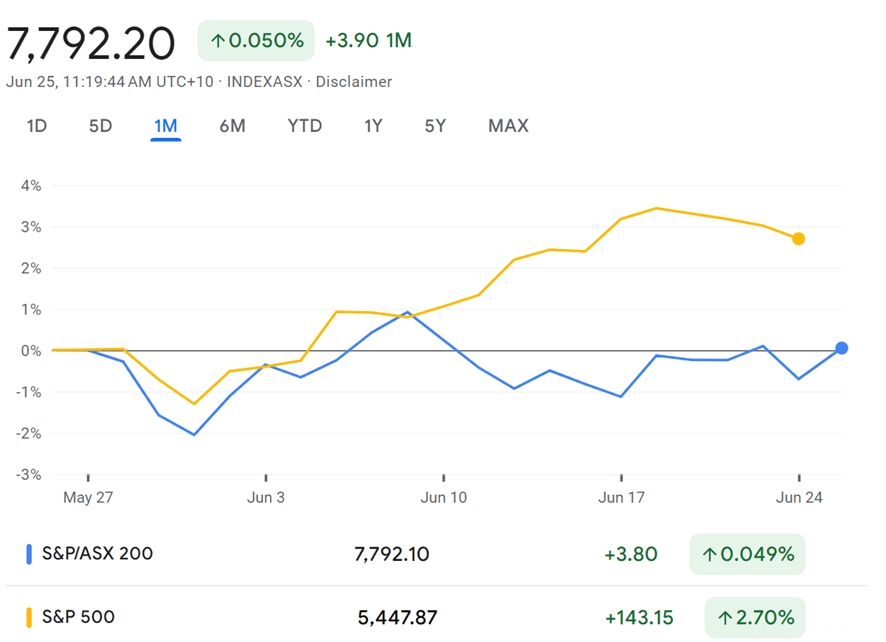

Placing the two indices side by side, we can see that the S&P 500 and Australia's ASX200 exhibited different performance patterns, reflecting the unique characteristics of their respective markets.

Both indices faced their own set of challenges and influences. The S&P 500's performance was affected by concerns about market exhaustion, especially in the tech sector, and investors' anticipation of upcoming economic data. The ASX200, on the other hand, navigated through pressures from consumer price index increases and the RBA’s interest rate decisions.

Despite these differences, both indices demonstrated overall positive movements, albeit at different scales. The S&P 500's gains were more substantial, while the ASX200's growth was more moderate but consistent. This divergence in performance highlights the distinct economic conditions, sector compositions, and investor sentiments in the U.S. and Australian markets during this period.

The Residential Property Market

The Australian residential property market demonstrated continued resilience through May and June 2024. Despite high interest rates and persistent inflationary pressures, housing values have continued to rise, driven largely by the significant imbalance between supply and demand.

Major Markets Performance

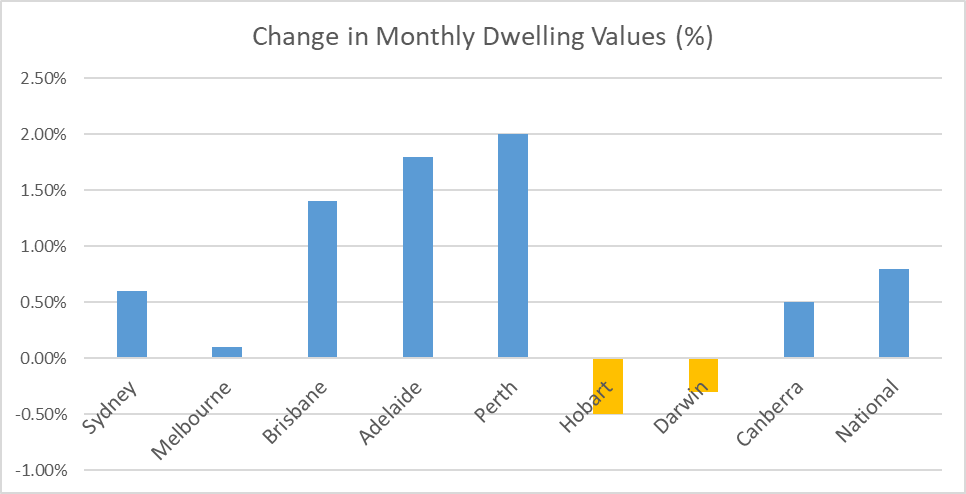

The recent trends in the Australian housing market show a varied pattern of growth and decline across different cities and regions. While some capital cities have experienced modest growth, others have seen slight decreases. The combined capitals and regional areas have both shown an overall increase, with the national average reflecting a positive trend. The median values of properties also differ significantly, with the highest being in the major cities and a lower median value in regional areas, indicating a diverse and dynamic real estate landscape across the country.

- Sydney: Sydney saw a moderate increase in property values, with a monthly rise of 0.6% and an annual increase of 7.4%. The total return for the year stood at 10.6%, reflecting steady growth in this major market.

- Melbourne: Melbourne's market experienced minimal growth, with a monthly change of 0.1% and a slight decline of 0.2% over the quarter. Annual growth was modest at 1.8%, with total returns reaching 5.5%.

- Brisbane: Brisbane outperformed most capitals with a significant annual growth rate of 16.3% and a strong quarterly performance of 3.9%. The median value in Brisbane reached $843,231.

- Adelaide and Perth: Both cities reported substantial annual growth rates of 14.4% and 22.0%, respectively. Perth, in particular, showed the highest growth among the capitals, reflecting a strong local market.

- Hobart and Darwin: Hobart saw a slight decline of 0.5% over the month and remained relatively stable over the quarter. Darwin experienced minor fluctuations but maintained positive annual growth of 3.5%.

- Canberra: The market in Canberra displayed steady growth with a 0.5% increase over the month and 2.0% over the year.

Regional Markets

Regional markets also demonstrated positive trends, albeit at a slower pace compared to capital cities. The combined regional index rose by 0.7% in June, bringing the annual growth rate to 5.9%. This performance indicates a continued interest in regional living, although the gap between capital city and regional growth rates has widened.

Factors Influencing the Market

Several key factors have contributed to the sustained growth in the housing market:

- Population growth: Continued strong immigration has increased housing demand, particularly in major cities.

- Limited supply: Despite efforts to increase housing stock, supply constraints persist, putting upward pressure on prices.

- Interest rates: While interest rates remain relatively high, there are expectations of potential cuts in the latter half of 2024, which may be supporting buyer confidence.

- Rental market pressure: Tight rental markets across the country are encouraging more first-time buyers to enter the property market.

Challenges and Concerns

Despite the overall positive trends, some challenges and concerns persist in the Australian housing market:

- Affordability issues: Continued price growth is exacerbating affordability concerns, particularly for first-time buyers in major cities.

- Potential for market correction: Some analysts warn of the risk of a market correction if interest rates remain high or economic conditions deteriorate.

- Regional disparity: The widening gap between capital city and regional market performance may lead to increased inequality in housing opportunities.

Outlook for the Remainder of 2024

The outlook for the Australian housing market for the rest of 2024 remains generally positive, with expectations of continued growth, albeit at a potentially slower pace. Factors such as population growth, supply constraints, and possible interest rate cuts are likely to support the market. However, affordability concerns and economic uncertainties may moderate the growth trajectory in some areas.In conclusion, the May-June 2024 period has seen continued strength in the Australian residential property market, with capital cities leading the growth. While challenges persist, the market has demonstrated resilience and adaptability in the face of changing economic conditions.

Inflation and Interest Rates

In June 2024, the Reserve Bank of Australia (RBA) decided to maintain the cash rate at 4.35%, a level it has held since November 2023. This decision comes amidst ongoing concerns about inflation and economic stability in the country.

Interest Rates

The RBA's decision to keep the cash rate steady at 4.35% reflects a cautious approach to monetary policy. The central bank has been vigilant about inflation risks, which remain a significant concern despite recent economic data showing mixed signals. The cash rate, which influences borrowing costs across the economy, has been a critical tool for the RBA in managing economic activity and inflation.

Inflation

As of June 2024, Australia's inflation rate stands at 3.6%, which is above the RBA's target range of 2-3%. The central bank has acknowledged that the process of returning inflation to the target range is unlikely to be smooth. Recent data indicates that while inflation has decreased from its peak in 2022, the pace of decline has slowed, suggesting persistent inflationary pressures in the economy.

Economic Context

The Australian economy has shown signs of slowing growth, with the first quarter of 2024 recording a meager 0.1% growth rate. Additionally, wage growth and the labor market have been weakening gradually, which aligns with the RBA's forecasts and the intended effects of previous interest rate hikes. The unemployment rate has also ticked up slightly to 4.0%, the highest level in two years, indicating some easing in the labor market.

Future Outlook

The RBA has indicated that it remains open to further rate hikes if inflationary pressures persist. However, the central bank also noted that the path to achieving its inflation target remains uncertain and that it will continue to monitor economic data closely. The next significant data point will be the consumer price inflation for the June quarter, which will provide a more comprehensive view of the inflationary trends and is expected to be available by the end of July.

Market Reactions

The financial markets have responded to the RBA's decision with a slight increase in the Australian dollar and a reduction in the probability of a rate cut by the end of the year. Economists and market analysts are closely watching the RBA's statements and future meetings, particularly the August meeting, which is seen as a potential point for policy adjustments depending on the inflation data.

Conclusion

The RBA's decision to hold the cash rate at 4.35% in June 2024 reflects a balanced approach to managing inflation and supporting economic stability. While inflation remains above the target range, the central bank is cautious about making further rate adjustments until more comprehensive data is available. The economic outlook remains uncertain, and the RBA's future actions will depend heavily on upcoming inflation and economic performance indicators.